Alternative Data – The Key To Making Informed ESG Investment Decisions?

Historically investors have used corporate disclosures of their environmental, societal and governance (ESG) related initiatives to assess ESG performance – but there is still much debate about what kind of data ESG performance reports should include.

The lack of globally standardized ESG reporting regulation means that corporate ESG performance reports vary widely in terms of consistency, quality and timeliness, while many investors, both institutional and retail, consider the data currently available to be largely insufficient. It is impossible to achieve higher risk adjusted returns, fulfil ESG mandates and increase the ESG levels of a portfolio by applying such data. It is no wonder that investors looking to gain greater and more impactful ESG exposure, often struggle to make meaningful buy, hold, or sell decisions based on this data.

IOSCO’s recent ESG ratings and data products report highlights the implications of inaccurate, unchecked reports for both companies and investors, which could “possibly lead to poor investment decisions on the part of the investor paying for and using ESG ratings or data products that are based on erroneous or limited information.”

It is essential that investors are able to assess how the available ESG performance data performs against four criteria. The first is reliability: ESG performance data needs to be accurate and the source verifiable. The second is granularity: consistent ESG performance data is required on a global scale if investors are to compare companies and peers meaningfully. The third is timeliness: real-time ESG event reports are essential when assessing ESG performance appreciation or degradation. The fourth is actionability: ESG performance data needs to be immediately actionable, supporting a buy, hold or sell investment decision.

Real-time analysis made possible

Every minute, corporate and non-corporate disclosures of ESG performance are published on social media, news channels, forums, and blogs. These disclosures report events that relate to ESG issues (such as companies that have been impacted by water shortage conditions or who have broken child labor laws).

In today’s world, where it is easier than ever to access the internet and device usage is at an all-time high, forums, blogs, and channels like Twitter have all become sites where almost anyone can discuss ESG-related issues. Of course, these wide-ranging sources differ in reliability – in our world of fake news, we are all aware of the need to fact check. It is only thanks to machine learning models that we can efficiently filter the credible from the noise.

From a granularity perspective, machine learning can also prove useful when it comes to ESG assessment. Unlike corporate sustainability reports and corporate filings that often refer to ESG performance in different ways, machine learning models can apply the same ESG taxonomy (that draws from other ESG standards) across all its assessments. These models can therefore evaluate ESG event reports in a more consistent and clear way.

One of the challenges is that ESG reporting available from sources such as corporate sustainability reports can have embedded time lags which makes ESG screening challenging. Timeliness and actionability are also resolved by machine learning technology as online reports of ESG event reports can be captured immediately.

Factors that will inform investor decisions (such as a company’s materiality, ESG performance appreciation or degradation and position relative to its peers) can therefore be evaluated more accurately, and in real-time.

Keeping investors ahead of the curve

The speed with which machine learning technology can detect and act is a huge benefit, especially given the rate at which ESG events develop, seemingly from nowhere. We need just think of the recent underwater gas pipeline leak off the Mexican peninsular. By the time the fire had been fully extinguished (a mere five hours, according to state oil company, Pemex), videos of the “eye of fire” had gone viral. ESG issues are fast-moving; reports and their evaluation need to keep apace.

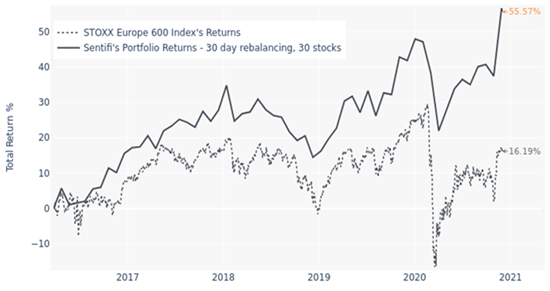

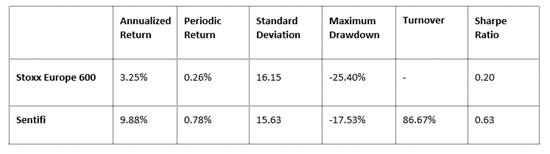

The illustration below outlines how alternative ESG performance data (i.e., data sourced by machine learning models from twitter, news and blogs) can be used to construct a portfolio of companies with strong positive momentum around their ESG performance. Rebalanced every 30 days, the portfolio consists of 30 companies from the STOXX Europe 600 index. These are companies that are selected on account of their positive ESG performance changes, as reported in social media, news, and blogs. They are that are outperforming a benchmark. Note how the annualized return for Sentifi’s ESG performance momentum strategy was 9.88%, as opposed to the benchmark of 3.25%.

Illustration 1: Portfolio construction based on ESG performance in twitter, news and blogs

Such statistics prove that alternative data really is the key to making meaningful investment decisions, not just at a theoretical level, but in practice, too.

Alternative ESG performance data, when sourced and assessed by machine learning technologies, enables investors to not only raise a portfolio's ESG level, but also focus on an increased risk-adjusted performance. In a world of progressively more and more environmental disasters and greater emphasis on ESG risks, alternative data should be a weapon that more investors consider for their arsenal.

**********

Marina Goche is CEO at Sentifi

***

The views expressed in this article are those of the author and do not necessarily reflect the views of AlphaWeek or its publisher, The Sortino Group

© The Sortino Group Ltd

All Rights Reserved. No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or scanning or otherwise, except under the terms of the Copyright, Designs and Patents Act 1988 or under the terms of a licence issued by the Copyright Licensing Agency or other Reprographic Rights Organisation, without the written permission of the publisher. For more information about reprints from AlphaWeek, click here.