Geography Based Investing if De-Globalization Persists

Institutional investors have a penchant for categorization and a seeming dislike of standardisation. It is not unusual for alternatives investors in particular to use asset, strategy, vehicle-type, or liquidity to bucket investments and assign staff responsibility. Geography is one of the key lenses that investors use, but is also not standardised. In most cases it is the region where the invested assets sit, but in some instances it is the manager domicile (which may give a differentiated approach). Against this siloed methodology, one needs to consider the fact that the globalisation of the world has increasingly blurred the lines on the asset side, especially as relates to multi-national corporations that derive their revenues from many regions and have global capital structures.

A reversal in the strong globalization trend that has persisted over the last decades needs consideration. While those outside of the US will quickly point to US partisan politics as the driver, what is important here is the effect de-globalization will have on investors’ views on geography specific investment as an alpha and diversification source.

From an investment standpoint, globalization has existed since the beginning of commerce. The movement of product across shifting national borders to broaden the consumer base has been key to forging a developed world and has been generally viewed as lifting societies, although clearly not equally.

In the alternatives world, particularly in hedge funds and private equity, those that were quick to identify more favorable risk/reward from a global palette have been able to outperform peers in returns and in turn to increase AUM without diminishing performance. Twenty years ago as the migration of alternatives really took hold outside of the US and Europe, there were many more hurdles, often jurisdictional/rule of law, that had to be taken on as risk or mitigated before prudent investment. Today capital is much more free-flowing and there is less concern surrounding the ability to divest from, as opposed to invest into, certain geographies as desired.

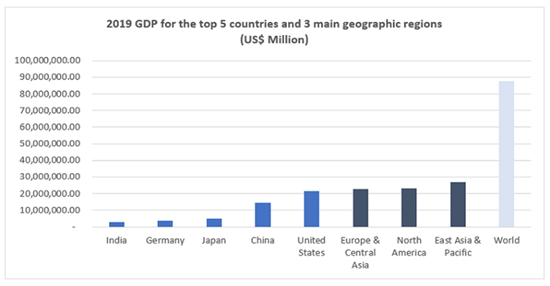

Source: World Bank.

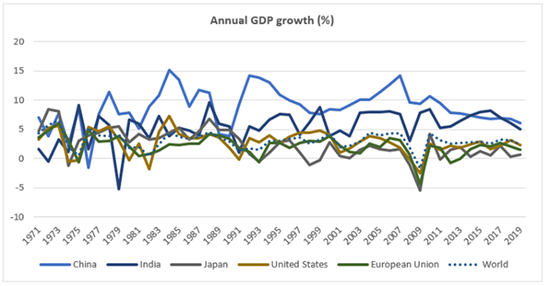

Source: World Bank.

While trade wars and protectionism are not new, the global pandemic is giving de-globalization a real boost. Governments are now focused on protecting their citizens, not just from Covid-19, but from reliance on outside supply chains. For some the pandemic might seem a convenient excuse for this activity, for others a necessary step, but regardless it is occurring. The US partisan divide might indicate a somewhat binary globalization outcome, but the Democrats seem to have adopted some of the protectionist views as the current administration despite disagreement on most else. US views towards China seem at present fairly united, but post-election greater differentiation may emerge. Brexit seems a distant memory but is perhaps indicative of further fracturing within Europe. While the crystal ball is a bit cloudy, there is more movement in support of a less globalized world and this has a potentially divergent effect on regional investment.

Let’s consider different regions:

Greater China

China’s economy is a behemoth and has left many a global CEO frustrated at not being able to get anywhere near the access provided to them by other major economies. It has also provided an interesting landscape for alternative investors. The confluence of US-China trade tensions, the pandemic and supply chain concern, as well as the China Communist Party asserting itself in places like Hong Kong blur the investment outlook. The impact of China’s continued nationalistic/imperialistic behaviours, including the Belt and Road initiative, provides perhaps the largest investment risk and thus opportunity sets. The question is does de-globalization narrow to de-Chinaization with support from the US and other large developed economies? A move towards de-Chinaization by the US and adopted by other G-20 nations would have huge ramifications going forward.

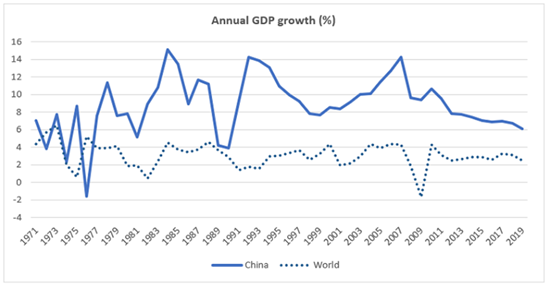

Source: World Bank.

Japan

Japan remains a fundamental market with distinct construct advantages for astute long/short investors, including the lack of institutional coverage of a majority of companies. Japan may get an additional boost from a more insular China and thus attract more investment coupled with increasing volatility from which to extract alpha.

Balance of Asia

The supply chain issue with China has clearly benefited other Asian geographies and this trend will likely support the investment case for emerging Asia. India, with its large population is trying to clean up on various fronts to become more of a global investment target, although development in alternatives away from PE seem to be slow in arriving at scale.

Europe

The state of the EU, including Brexit, has been overshadowed by the pandemic. Trade tensions with the US are real and although less critical than those with China, are likely to persist. This has implications across asset classes as the ECB attempts to prop up the Eurozone with the aim of achieving a more V-shaped recovery.

US

The US is likely to remain the investment capital of the world and it has been the view for some time that US equity markets are being treated by the world as a secure money market instrument. Ebullient US equity markets however are disconnected from fundamentals and this, at some point, will necessarily cause a reassessment of value. Should US nationalism be given a further impetus with Trump and GOP Senate victories it is unclear as to the “go it alone” valuation sustainability. On the flip side, it would seem that at least an increase in volatility associated with a new administration, replete with expected higher taxes and new regulation, will need to be priced into equities and credit.

Emerging Markets (ex-Asia)

It is interesting to contemplate the potential effect of de-globalization on emerging economies reliant upon developed nations as trading partners. It is obvious that a recessionary state of developed economies cannot be beneficial to the emerging ones, but it is less clear as to the benefit/detriment of de-globalization in a stable economic environment, let alone a recessionary one.

EM investors have long been cognizant of the importance of country and region selection for risk assessment. This top-down approach to geography in a de-globalizing world may play a more important role across the investment spectrum, including in leading economies. The careful analyses of impacts to each region has its roots in macroeconomics but really rests on an investors ability to pick those regions where the “action” is likely to be for an extended period, thus creating better risk-adjusted opportunities.

Once the geography has been chosen, it is imperative to find the manager with the highest probability of extracting alpha from the opportunity set. This involves all the normal top-down and bottom up manager selection, but with the added burden of assessing regional expertise, cultural biases, and jurisdictional issues.

Using a top-down geographic lens for trying to maximize alpha is sure to be influenced by a continued move towards de-globalization. As nationalism has emerged in multiple jurisdictions, it seems unavoidable that a universal result will be a slowing or unraveling of globalization. Some of this is a reaction to supply chain concerns, while attempting to repatriate production is seen as solid economic policy. Inevitably there will be resultant winners/losers, as well as a shifting rule of law, as governments deal with the derivative effects of this groundswell. De-globalisation may end up being predominantly an anti-China story, but it is likely too early to call a halt of capital in/out of Greater China. Investors should use multiple lenses to attempt to develop portfolios designed to be all-weather and which can function well in a variety of scenarios whatever the future trajectory of globalisation.

**********

Jim Neumann is Partner and Chief Investment Officer at Sussex Partners

***

The views expressed in this article are those of the author and do not necessarily reflect the views of AlphaWeek or its publisher, The Sortino Group

© The Sortino Group Ltd

All Rights Reserved. No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or scanning or otherwise, except under the terms of the Copyright, Designs and Patents Act 1988 or under the terms of a licence issued by the Copyright Licensing Agency or other Reprographic Rights Organisation, without the written permission of the publisher. For more information about reprints from AlphaWeek, click here.