Japanese Hedge Funds Review And Outlook 2022/23

Perhaps not entirely surprisingly given the global backdrop, 2022 was yet another challenging year for Japanese hedge funds on an absolute return basis (though not on a relative basis) with the average manager in the HFRI Japan Index returning +0.3% through September of last year. Of course, one could take the view that any positive return last year is a significant achievement, and it certainly shows once again that Japanese hedge funds as a group have been able to weather the storm better than their global peers; through the end of September, the EurekaHedge North America Long Short Equities Hedge Fund Index was down -13.7%.

Significant performance dispersion amongst managers and trading styles, however, has continued. Market neutral managers, and in general strategies for which fundamental analysis plays a key role, especially those focused on longer term investment horizons, continued to struggle to generate meaningful absolute returns last year. Dispersion among these types of managers has been particularly significant, with some managers up over +20% YTD as of September and others nursing losses in the mid-teens for the same time period. Those with a meaningful value tilt seem to have done better, though often on the heels of prior years of significant underperformance when value was very much out of favor due to quantitative easing which pushed up growth names instead.

Once again, this is very much in line with the challenges faced by managers globally in 2022, with the difference to 2021 being that while many equities-focused hedge funds have struggled to generate significant absolute returns, they have generated significant alpha versus their underlying indices. We have also seen some green shoots in terms of fundamentals starting to matter once more to investors. We expect this importance to become even more pronounced as liquidity continues to be drained from markets, interest rates continue to increase, and investors finally realize the importance of company profitability once again. As we have commented on in previous years, those Japanese manages unable/unwilling to adapt to the current environment and who stick to their long-term approaches are amongst those that continue to struggle the most. In the long run they may be vindicated, but we have seen substantial AUM drops for some of those managers in the meantime, and hence sticking to their guns could turn out to be a costly exercise for them both in terms of performance and their overall businesses.

Trading oriented/multi-pm funds have generally done better, with returns in the low single digits to low teens through September of 2022. The issue here though remains the same as before in that there is both a lack of capacity as well as a lack of institutional grade (in a global sense) managers that are available for investment.

2022 validates our view that holding a diversified portfolio of Japanese managers would have insulated investors to some extent from manager-specific volatility and provided investors with smoother returns, notwithstanding the above-mentioned caveats of capacity and infrastructure which make investing in Japan challenging for all but the most sophisticated allocators with deep knowledge of the Japanese hedge fund industry.

As we have done in previous years, this year’s report updates and compares Japanese hedge funds as a group with their long only benchmarks as well as with their North American and European peers. This allow investors to judge relative performance and assess whether the added layer of fees and lesser liquidity that invariably come with hedge fund investments are justified.

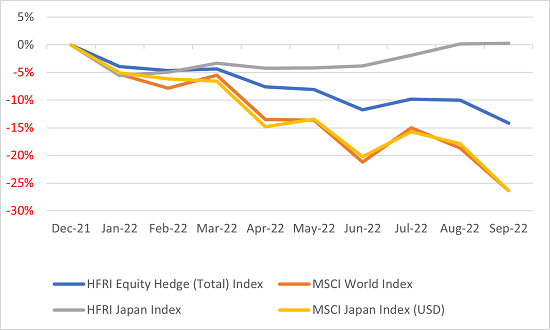

After underperforming the HFRI Equity Hedge (Total) Index in 2021, the HFRI Japan Index significantly outperformed it last year. The outperformance versus both the MSCI Japan and the MSCI world indices is even more stark, showing that Japanese hedge funds as a group materially protected capital in 2022 versus long only. While Japanese hedge fund as a group were flat (+0.3%), both MSCI indices lost -26.4% during the same period.

Figure 1: Cumulative Returns, Public Equity vs Hedge Funds, 2022 Through September

Source: HFR, MSCI

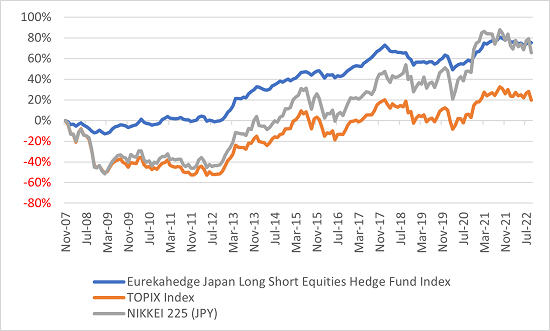

Again, as in previous years, we have also looked at the longer-term comparison of the Eurekahedge Japan long/short hedge fund index versus the TOPIX and the NIKKEI 225 indices (see figure 2).

Since 2007, Japanese hedge funds as a group have marginally outperformed both the TOPIX and the NIKKEI indices on an absolute basis but have significantly outperformed on a risk adjusted basis. While the TOPIX index suffered a maximum drawdown of -53.03% and the NIKKEI 225 index a maximum drawdown of -51.74%, the Eurekahedge Japan index only lost 13.72% over the same period. It is also interesting to observe that these maximum drawdowns occurred during different periods (May 2012 for the TOPIX Index, February 2009 for the NIKKEI 224 Index and March 2020 for the Eurekahedge Japan index). The volatility profile of Japanese hedge funds is also much more benign, coming in at 5.68% versus 17.93% and 19.48% for the TOPIX and the NIKKEI 225 indices respectively. This shows that Japanese hedge funds continue to be a much better risk adjusted way to invest in Japan than through long only funds, even after taking into account the higher fees and lesser liquidity.

Figure 2: Historical Cumulative Performance of Equity Hedge Funds Relative to Public Equity

(December 2007 - September 2022).

Source: Eurekahedge, Bloomberg

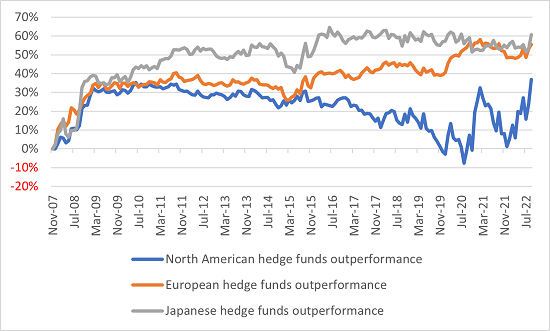

Japanese hedge funds as a group continue to show the largest outperformance over time versus their equity benchmarks and their North American and European peers and this cumulative outperformance has further improved last year (see figure 3). However, North American hedge funds have narrowed the gap somewhat, owing to the big losses in North American equity indices last year (the MSCI North America index is down -25.5% YTD) versus the more muted losses among North American hedge funds (the Eurekahedge North America Long Short Equities Hedge Fund Index is down -13.7% during the same period). The big difference, of course, being the fact that Japanese hedge funds have made a return last year, albeit small, whereas North American hedge funds have lost money in 2022 so far. It is still striking to see how consistent the long-term gap remains between Japanese hedge funds and their North American peers. While North American equity-oriented hedge funds continue to represent the single largest part of the hedge fund industry, Japanese hedge funds continue to be but a small sliver of the overall industry AUM. Given their consistent alpha generation it would perhaps make sense for investors to consider allocating more to Japanese and less to North American equity hedge funds.

Figure 3: Historical Cumulative Outperformance of Equity Hedge Funds vs Equity

(December 2007 - September 2022)

Data: North American equities = Eurekahedge North American Hedge Fund Index vs. MSCI North America Index (USD), European equities = Eurekahedge European Hedge Fund Index vs. MSCI Europe Index (EUR), Japanese equities = Eurekahedge Japan Hedge Fund Index vs. MSCI Japan Index (JPY).

Source: Eurekahedge, MSCI

The alpha opportunity for Japanese hedge funds seems to have continued uninterrupted, though the headwinds the industry faces (limited capacity, limited number of funds, language and cultural barriers and less institutional grade firms) haven’t changed in recent years. Perhaps a resurgence in travel to Japan and continued strong performance will help to ease these bottlenecks over time.

**********

Patrick Ghali is Managing Partner at Sussex Partners

***

The views expressed in this article are those of the author and do not necessarily reflect the views of AlphaWeek or its publisher, The Sortino Group

© The Sortino Group Ltd

All Rights Reserved. No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or scanning or otherwise, except under the terms of the Copyright, Designs and Patents Act 1988 or under the terms of a licence issued by the Copyright Licensing Agency or other Reprographic Rights Organisation, without the written permission of the publisher. For more information about reprints from AlphaWeek, click here.