Japanese Hedge Funds Review And Outlook 2023/4

2023 has been a year dominated by macro factors, especially the perceived path of global rates, and particularly the US. This dynamic has been the main driver for equity markets in Japan and has created a challenging background for active managers, notably those focused on deep fundamental research. Given that the Japanese hedge fund industry continues to be somewhat biased towards low net exposure fundamental managers (in other words, alpha heavy strategies), any environment which is driven by macro flows rather than idiosyncratic/company specific factors creates headwinds and challenges. The same constraints, of course, also applied to hedge funds in other geographies this year and it is interesting to see that, despite this, Japanese hedge funds as a group have once again outperformed their North American peers (+4.9% through the end of October versus +2.2% respectively for the same period as measured by the measured by the Eurekahedge Japan Hedge fund index and the Eurekahedge North America Index).

Performance dispersion also continued this year. Long biased managers, or those with more flexible net exposure management and/or the ability/willingness to run with larger net long exposures, have done significantly better at capturing market beta this year, with some generating double digit returns YTD. However, those managers who came into the year defensively positioned, a tactic which served them well last year, have not participated in the (albeit very narrow) rally in Japanese markets. The macro flows driving this year’s markets also led to significant flow and factor rotations of growth versus value (most recently again in October/November of this year). The fact that many Japanese growth stocks tend to be small caps further limited the opportunity for hedge funds to participate, due to their inherent volatility and often questionable fundamentals. For an industry where many PMs remain biased towards fundamental analysis, getting comfortable with such positions is therefore challenging. Additionally, managers were also all too aware of the violent short squeeze risk in a non-fundamentals driven market, which further limited their willingness to engage.

Managers that were not exposed to very specific companies consequently weren’t able to capture this year’s upside in any significant manner, which was not dissimilar to the situation in the US where 7 stocks drove most of returns so far in 2023. Until such a time as markets are driven by fundamentals again, the opportunity set for long/short equity hedge funds globally, especially those narrowly constrained in their net and factor exposures, may continue to be limited. Once there is more clarity on the path of global rates, the environment for these types of strategies should significantly improve.

Longer term structural changes in Japan, such as the improved treatment of shareholders, the restructuring of the Tokyo Stock Exchange and pressure being put on companies to increase dividends, are all tailwinds that should remain with the industry for years to come. Some managers feel this will provide an opportunity for the next 10 years, and though on the face of it this may seem like an argument for a long only approach to Japan, this should also provide plenty of short opportunities for managers.

The resurgent interest in Japan more broadly has certainly also led to more inbound enquiries for Japanese hedge fund managers. It appears, however, that international investors may still not fully grasp the alpha opportunity that the Japanese markets provide and instead seem very much focused on factors favoring long only strategies. Themes such as shareholder engagement are certainly very trendy with foreign allocators, but they are often surprised to find that Japanese hedge funds, though aware of this trend, are not solely focused on this and rarely will make it their core theme. There continues to be a disconnect, therefore, between the expectations of foreign investors and where local managers see the best opportunities. The resulting risk presented by this is that foreign flows may reverse, as they have done in the past, should the current upward trajectory in markets reverse, which could accelerate declines. Perhaps a more prudent approach would be for allocators to focus their research efforts on understanding the inherent alpha opportunities that Japanese hedge funds can provide.

In terms of more granular performance attribution, just as in prior years, multi-pm funds have generally done better. The issue here though remains the same as before in that there is both an extreme lack of capacity as well as a lack of institutional grade (in a global sense) managers that are available for investment.

Last year’s comment therefore remains valid also in 2023:

“2022 validates our view that holding a diversified portfolio of Japanese managers would have insulated investors to some extent from manager specific volatility and provided investors with smoother returns, notwithstanding the above-mentioned caveats of capacity and infrastructure which make investing in Japan challenging for all but the most sophisticated allocators with deep knowledge of the Japanese hedge fund industry. “

Every year we compare Japanese hedge funds as a group with their long-only benchmarks as well as with their North American and European peers. This allows us to judge their relative performance, and their net of fee value add versus cheaper long only investment.

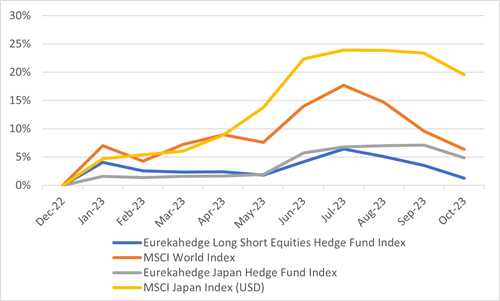

After significantly outperforming both the MSCI Japan and the MSCI World indices last year, and materially protecting capital in 2022 versus long only investments, (Japanese hedge funds as a group were roughly flat in 2022 at +0.3% while both MSCI indices lost -26.4% during the same period), 2023 has painted a somewhat different picture. While Japanese hedge funds measured by the Eurekahedge Japan index were up +4.9% through the end of October, the MSCI Japan and the MSCI Word index were up +19.5% and +6.3% respectively. Hedge funds have therefore not kept up with their long only benchmarks this year, which can be attributed to the aforementioned reasons

Figure 1: Cumulative Returns, Equity vs Hedge Funds, 2023 Through October

Source: Eurekahedge, MSCI

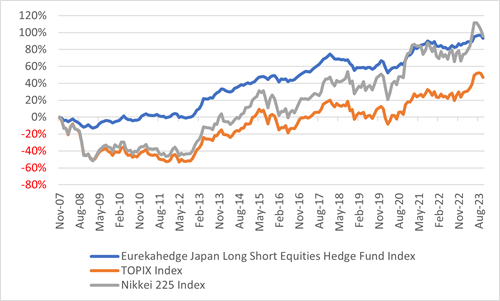

Longer term (since 2007), and despite this year’s rally, Japanese hedge funds as a group have significantly outperformed the TOPIX index and have generated returns which are comparable to the Nikkei index on an absolute basis. Importantly though, they have significantly outperformed both indexes on a risk adjusted basis (see Figure 2). While the TOPIX index suffered a maximum drawdown of -53.03% and the NIKKEI 225 index a maximum drawdown of -51.74%, the Eurekahedge Japan index only lost -12.76% over the same period. The volatility profile of Japanese hedge funds is also much more benign at 5.69% versus 17.58% and 19.19% for the TOPIX and the NIKKEI 225 indices respectively. Japanese hedge funds therefore have continued to provide a much better risk adjusted way to invest in Japan (net of fees!).

Figure 2: Historical Cumulative Performance of Equity Hedge Funds Relative to Equity (December 2007 - October 2023)

Source: Eurekahedge, Bloomberg

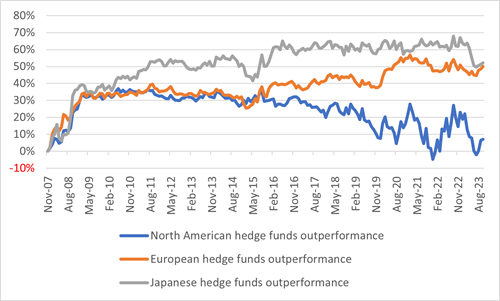

This year has seen a further increase in the gap between the cumulative outperformance versus equities of Japanese Hedge funds and their North American peers, while European funds have managed to retain their performance (see Figure 3). This is perhaps not unsurprising given the very narrow breadth of the rally in US markets, and the challenges this posed for long/short managers. It does, however, highlight once again that selecting the markets in which to allocate to hedge funds makes a significant difference in terms of value-add. Japan continues to be the standout in that regard, with the long-term gap between Japanese hedge funds and North American peers persisting.

Figure 3: Historical Cumulative Outperformance of Equity Hedge Funds vs Equity (December 2007 - October 2023)

Source: Eurekahedge, MSCI

Data: North American equities = Eurekahedge North American Hedge Fund Index vs. MSCI North America Index (USD), European equities = Eurekahedge European Hedge Fund Index vs. MSCI Europe Index (EUR), Japanese equities = Eurekahedge Japan Hedge Fund Index vs. MSCI Japan Index (JPY).

As the world rightly continues to rediscover the opportunities presented by Japan, allocators must be careful not to myopically focus on the recent upward momentum in Japanese markets, and hence only look at long only strategies, but to recognize the compelling long-term alpha opportunity the local hedge fund industry presents.

**********

Patrick Ghali is Managing Partner at Sussex Partners

***

The views expressed in this article are those of the author and do not necessarily reflect the views of AlphaWeek or its publisher, The Sortino Group

© The Sortino Group Ltd

All Rights Reserved. No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or scanning or otherwise, except under the terms of the Copyright, Designs and Patents Act 1988 or under the terms of a licence issued by the Copyright Licensing Agency or other Reprographic Rights Organisation, without the written permission of the publisher. For more information about reprints from AlphaWeek, click here.