The Never Ending Recovery Of Natural Gas

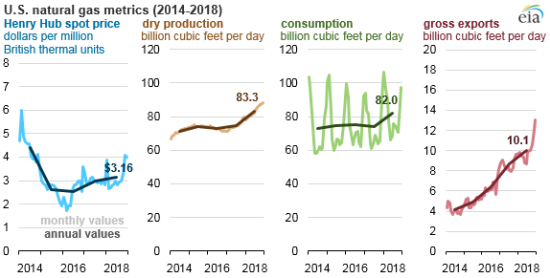

Natural gas prices witnessed a rise of 50% followed by an approximately 50% plunge in the winter of 2018/19. The commodity suffers from a never-ending recovery from the great shale hangover ten years ago. In 2018 U.S. consumption rose by 7 billion cubic feet per day (Bcf/d) compared to 2017 but dry gas production also increased by 8 Bcf/d, and prices as of February ended up where it was a year ago. If the brutal winter we just came off did not even cause lasting effect on prices, are we destined for another boring year for gas?

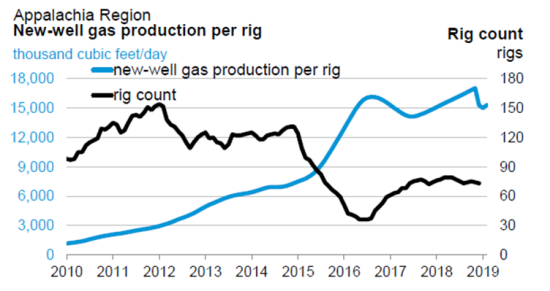

The story of technological advance in shale oil and gas is extraordinary. As recently as 2015, a great gas well is one that averages 5 million cubic feet per day (MMscf/d); today a monster well in the Appalachia clocks in at 15 MMscf/d routinely. The U.S.’s single year production increase of 8 Bcf/d represents half of all volumes produced in Canada. However, this productivity gain has flattened out; and there are good reasons to believe that gas, as well as oil producers, have begun to hit a wall on packing more wells into a single drilling pad, lengthening the drills, and using more frack sand and water. Since hitting a peak in October 2018, production has flatlined. Gas drilling has not yet been affected by lower oil prices but it is expected, and that has a lagging effect that will show up a few months down the road.

Stellar export growth, especially to Mexico, in 2018 was a big story and with continued significant LNG capacities coming online in 2019 overall export is projected to grow by another 3 Bcf/d. Granted, some of these volumes are tied to short term contracts., but worldwide buyers of LNG tend to be big-volume consumers with long term, stable demand projections. There is little room for surprise.

Storage level is tracking 5-year low following big draws in November and January. While weather patterns in the Northeast U.S., where heating demand is the highest, are trending normal this spring, there are structural factors that point to bullish consumption patterns. According to a recent RBN Energy study, not only is petrochemical industrial demand picking up, temperature-adjusted demand for the past two years has also been trending up, indicating structural changes in the power sector related to increasing market share of gas-fired generation at the expense of coal and nuclear power plants. In fact, coal prices have been trending up all year to $35 per megawatt-hour (MWh) of power generated compared to that of natural gas at $20 as of this writing, encouraging higher gas utilization.

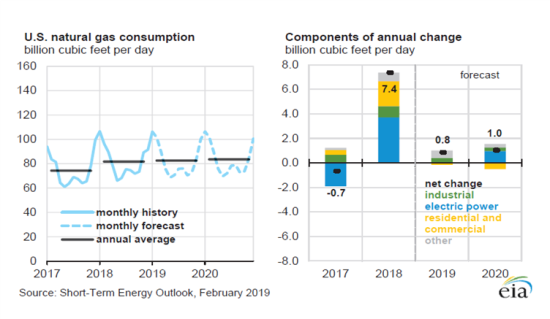

After a blockbuster year, the latest EIA outlook now forecasts only 0.8 Bcf/d net demand growth for 2019, resulting in a build in inventory back up to 5-year average. This assumes a slower pace of coal-to-gas switching and subdued summer cooling demand and normal winter demand. Given that half of all domestic demand growth last year came from power generation, this projection contains a significant upside price risk should we have a weather upset this summer.

Natural gas prices are so notoriously volatile it is sometimes called the widow maker. The recent violent drop was due solely to its sensitivity to weather changes. However, with a corresponding plunge in speculative money short to multi-year low, likely flattening of production growth in the coming months, the ferocity of price drop to 2.5-year low, and the promise of summer heat, there appears to be an asymmetric setup for natural gas for an upside surprise.

**********

Jeff Lee is Principal of Kronos Management

Opinions expressed in this document are for general informational purposes only and are not to be construed as an offer, recommendation, solicitation, or investment advice. Kronos Management makes no representation or warranty relating to any information herein, which is derived from independent sources. Trading commodities bears substantial risk of loss, and is not suitable for all investors. Please consider your financial condition prior to investing with Kronos. For further details regarding the risk of trading with Kronos, refer to the Disclosure Document.

***

The views expressed in this article are those of the author and do not necessarily reflect the views of AlphaWeek or its publisher, The Sortino Group

© The Sortino Group Ltd

All Rights Reserved. No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or scanning or otherwise, except under the terms of the Copyright, Designs and Patents Act 1988 or under the terms of a licence issued by the Copyright Licensing Agency or other Reprographic Rights Organisation, without the written permission of the publisher. For more information about reprints from AlphaWeek, click here.