Sizeable Hedge Fund Allocations Help Swiss Investors Through Covid-19 Market Tumult

Switzerland is often considered as one of the birth places of the hedge fund industry. Many of the earliest and most active hedge fund investors came from Switzerland, initially through its many innovative family offices and plethora of private banks, and later through the addition of institutional investors. Swiss money in many ways is a misnomer. It is estimated that as much as 62% of all money managed by Swiss banks is from customers domiciled abroad, and Switzerland is also estimated to be the most important cross border wealth management hub globally with a 27% market share[1]. Swiss investors have tended to maintain significant allocations to hedge funds, and allocations in the 20% range by wealth managers and family offices are not unusual. In addition to this, many Swiss institutions also currently maintain significant allocations. Against this backdrop, it is of course always interesting to see what local investment trends may look like, and to understand what the current appetite for hedge funds in Switzerland is.

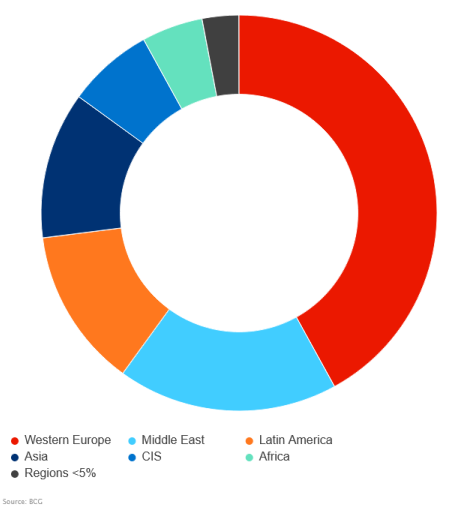

Fig.1

Swiss Wealth Management Industry AUM by Domicile

Over the past few years, we have seen somewhat of a bifurcation in local demand between very liquid investments (e.g. daily dealing UCITs funds) and illiquid private investments (e.g. direct lending). The drive towards more liquid, and regulated, UCITs investments is a result of multiple factors. There are still painful memories of funds’ having gated as a result of the global financial crisis with some investors holding side pockets as a remnant of this period to this day. Additionally, some custodian banks have been increasing trading fees on offshore funds, and taxation and distribution rules also make accessing such funds more difficult and costly for certain types of investors. The increase in number and quality of UCITs funds has also helped spur demand, and the often-daily liquidity these funds offer provide some investors with an additional sense of security.

Illiquid investments, on the other hand, have become very popular with longer term investors, as they appear, at least in theory, to shield investors from short term volatility and should provide some sort of illiquidity premium. With negative yields being a significant problem (not just for Swiss Franc-based investors) the promise of steady positive returns looks very attractive indeed. As a result, this has even led to some private wealth managers and banks structuring such products as alternatives to savings accounts.

Many Swiss investors have, over the last 18 months, started to explore, and increase, allocations away from traditional market betas. This was fueled by an uneasy feeling about the relentless bull market, and a perceived need to diversify away from traditional equity and credit exposures (some wealth managers had eliminated all negative yielding debt from their approved investment universes last year), as well as a need to find new sources of yield. The current crisis has clearly further accelerated this effort. Demand for an alternative to market beta, investments that offer convexity, and a reminder that illiquid private investments may not be as riskless as many investors have been led to believe, is leading to allocation shifts.

As a result, investors are currently both contemplating increases in their hedge fund allocations as well as changes to the composition of their hedge fund portfolios. These allocations and changes are both driven by recent performance of specific managers and strategies (the dispersion of manager performance within a given strategy so far this year being noteworthy), as well as newly emerging opportunities brought about by significant dislocations in specific market segments (e.g. parts of credit). These take the form of both non-correlated investment ideas, all weather type portfolios that should be able to generate returns in both up and down markets (or at the very least protect capital), as well as more directional recovery trades for which there is a significant amount of capital currently being raised by many of the best known managers.

Another trend is that many brand name managers have in the past few months reopened their funds for the first time in years to new capacity. Swiss private banks in particular have been busy raising significant capital to fill this capacity. The combination of perceived stability and safety coming from investing with some of the best-known names in the industry, performance and exclusive access has been a boon for these managers as well as for the banks able to sell this capacity.

It will be very interesting to see what type of impact the disappointing performance by certain credit related strategies (both hedge fund and direct lending/private debt) during this crisis will have in terms of local investor appetite. Questions now abound about fair valuations of their underlying assets as well as a what the lack of liquidity in a crisis really means in terms of risk. Sometimes questionable underwriting standards, in addition to some high-profile problems experienced and widely written about in local newspapers certainly don’t help. If nothing else, a significant reassessment and renewed diligence drive by investors in such strategies is certain. The current problems experienced by direct lending/private debt managers are very much reminiscent of what happened during the global financial crisis, where similar promises to investors had been made and where many investors underestimated the true risks they were exposed too, instead allowing themselves to be drawn in by the lure of seemingly steady and uncorrelated returns.

The problems caused by an increase of negative yielding instruments will not go away anytime soon though, and the current crisis has only exacerbated the issue. The pressure on investors to find alternative return sources will therefore only increase. Given that a somewhat carefully constructed portfolio of hedge funds has significantly outperformed the markets (as well as a typical 60/40 portfolio) so far in this current crisis, while often also providing liquidity, and that volatility is seen by many investors as being here to stay, hedge fund investments, together with active management in general, should continue to see an increase in interest by Swiss investors.

**********

Patrick Ghali is Managing Partner at Sussex Partners

Footnotes

- [1] Swiss Bankers Association website, 6th June 2020 https://www.swissbanking.org/finanzplatz-in-zahlen/wealth-management_e/

***

The views expressed in this article are those of the author and do not necessarily reflect the views of AlphaWeek or its publisher, The Sortino Group

© The Sortino Group Ltd

All Rights Reserved. No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or scanning or otherwise, except under the terms of the Copyright, Designs and Patents Act 1988 or under the terms of a licence issued by the Copyright Licensing Agency or other Reprographic Rights Organisation, without the written permission of the publisher. For more information about reprints from AlphaWeek, click here.