Active vs Passive Management

Actively and passively managed products are available across many different investment products, but as AlphaWeek covers the alternative investment industry and I work within the hedge fund segment of this industry, I’ll be looking at hedge funds as the active management investment vehicle. I will also focus the majority of the article within the equity hedge fund section of the industry.

As an executive summary of my active and passive management investment philosophy, I believe in:

- Paying low, passive fees for market risk, and other known risk factor, exposures;

- Paying performance fees for exposure to Beta/systematic risk-neutral exposures, such as:

- (i) idiosyncratic risk;

- (ii) new/not well-known factor risk(s), and

- (iii) alpha generation.

- I don’t believe in paying performance/active management fees for a high mix of exposure to systematic risk and other risks.

Figure 1: A breakdown of equity exposure vehicles and management types

Why is it difficult for active managers to consistently beat passive investment returns?

Active managers have two primary disadvantages, or hurdles, to get over in order to consistently beat passive returns. These two hurdles are the fund’s cash holding - which means less than 100% of active AUM is competing against 100% of passive AUM - and fees. How much do these hurdles affect parity, ceteris paribus?

To calculate an active manager’s return parity, I use the following assumptions: a traditional 10% of AUM cash position and a traditional hedge fund 2&20 fee model (2% management fee & 20% performance fee). In order to calculate parity, I used the S&P 500’s 2019 monthly returns for both active and passive returns. I also assumed a 25 basis-point fee as the cost to get exposure to the S&P 500 via an Index or ETF, for example the SPY. I have also included a 1&15 model, as average hedge fund fees have fallen in recent years.

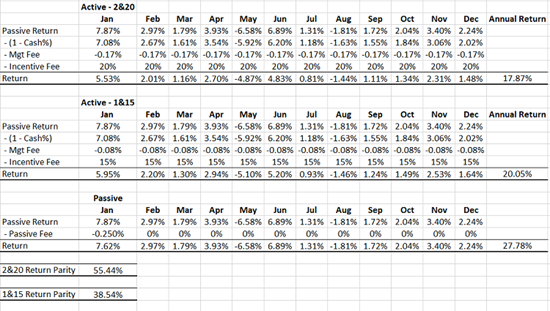

In 2019, hedge fund active managers with a 2&20 fee model needed to return an additional 55.44% on top of the passive investment’s gain in order to just break even on a net return basis versus the passive investment and those with a 1.5&15 fee structure needed 38.54% (see Figure 2 below). This, large, parity return needs to be earned every single year by the active managers just to break even. The two main tools that the hedge fund active managers have in order to make up this parity return are (1) the use of leverage - being able to use more than 100% of AUM, and (2) the ability to take on more types of risk than the passive investment strategy/product.

Source: Excel computation using the above return and fee assumptions

Market Theory Overview – EMH, CAPM, APT

At this stage, I think it's important to touch on the different market theories. In the 1960’s, Eugene Fama developed the Efficient Market Hypothesis (EMH) in his Ph.D. dissertation. The EMH essentially states that stock prices reflect all relevant information at all times and trade at exactly their fair value. This means that it is impossible to consistently beat the market and that choosing market-beating stocks is more about luck than judgement.

In 1964, William Sharpe developed the Capital Asset Pricing Model (CAPM). The CAPM is a single factor linear model that states that an asset’s expected return is equal to a combination of the factor of market risk to that asset and alpha.

The Arbitrage Pricing Theory (APT) developed by Stephen Ross in 1976 was developed as an alternative to the CAPM. The APT is essentially a multi-factor pricing model based on the idea that an asset's returns can be predicted using the linear relationship between the asset’s expected return and a number of macroeconomic variables that capture systematic risk.

The primary differences between the APT and CAPM are that the CAPM is a single factor model (market risk) and assumes an efficient market. The APT is a multi-factor model but believes there are short-term price dislocations before finding their way back to fair value.

The last model I want to reference is the Fama-French 3-factor model developed in 1992. Fama and French found that 3 different factors - the CAPM market factor, along with a size factor and value factor - better explains asset prices returns (this is a combination of CAPM and APT).

These theories are widely taught and widely used within the investment arena. In my opinion, all of them have their pro’s and con’s but none of them do a great job of really explaining asset prices. This is primarily due to the math and assumptions that go into the models, which I will explain in more detail in future posts, as well as changing market ‘factor’ dynamics.

Systematic Risk, Idiosyncratic Risk, Factor Risk

I also want to touch on the well-known different types of risks. They are:

- Systematic Risk/Market Risk

Macro factors that move the broad markets – APT has multiple factors (for example GDP, rates, unemployment) while CAPM has one. Systematic risk cannot be diversified away.

- Unsystematic Risks/Idiosyncratic Risks

Unique risks to individual stocks (for example Governance, product line, financial fraud, loss of Directors). Idiosyncratic risk can be diversified away; as the number of stocks increase in your portfolio, the idiosyncratic risk tends towards zero.

- Factor Risks

Fama & French found that value & size factors brought in risk-adjusted returns not driven by market risk. Carhart added a momentum factor to be a 4-factor model (1997) and Fama-French later developed a 5-Factor model (2013); Market, Size, Momentum, Profitability & Investment Patterns; Fama disagrees with Carhart’s momentum factor primarily in terms of its economic validity.

Passive & Active Management

My believe on investment into passive or active management is based on which type of risk(s) I want exposure to. I believe that low fees should be paid for systematic exposure, and other well-known factor exposures, in a passive management style, and active management/performance fees are only to be paid for concentration of both alpha and idiosyncratic exposures with low-no systematic exposure. That means, based on the following market theories:

- EMH

Systematic/Market Risk

I would invest in passive investments across all asset classes as all prices are always fair value.

Alpha

Within EMH, you cannot consistently beat the market and any market-beating strategies are just luck, therefore I would have no actively managed investments.

- CAPM

Systematic/Market Risk/Beta

I would invest in cheap, passive investments in the proxy of the market within each asset class.

Factor Risks

As CAPM only has one factor which is market risk above, there would be no investment in ‘other’ factors.

Alpha

Using CAPM, alpha is explained as the excess return of the market. As I already have market exposure via my passive investments, I would use active investment in market-neutral/low to no beta strategies that bring in returns unrelated to my passive market returns therefore concentrating on pure alpha returns.

- APT

Systematic Risk/Beta

Similar to the CAPM, I would invest in cheap, passive investments in the proxy of the market within each asset class.

Factor Risks/Betas

- I would have passive investment in the ‘cheap’ ETFs that exist bringing exposure to non-market factors like Fama-French’s 4 factors and Carhart’s momentum factor.

- I would have active management in exposure to new or unknown factors, to the wider public, that are market-factor neutral.

Alpha

Using APT, alpha is explained as the excess return of the factors. As I’d already have factor exposures via my passive investments, I would use active management in market-neutral/low to no beta strategies that bring in returns unrelated to my passive market returns.

Overall, I would have the majority of my investments in low-cost passively managed market and factor exposures across the different asset classes with a smaller allocation to risks/exposures that can be provided by active managers, for example hedge funds, to help further diversify the portfolio and add to the portfolio’s return in terms of alpha. According to my investment philosophy, passive investment already covers equity market risk and as I don’t want a strong overlap in exposure with my active management investment, I would not consider equity hedge funds that are heavily exposed to market risk, i.e. have a significant beta coefficient. Another reason, I do not want my active investment to have the same exposures of my passive investments is due to the significant hurdles that was spoken about at the beginning of the article.

In my next article, I will go into more detail on my specific hedge fund investment philosophy.

**********

Karl Rogers is Founder of ACE Capital Investments

Investment programs involve substantial risk, including the complete loss of principal, and no assurance can be given that the Fund’s investment objectives will be achieved. Past returns are no guarantee of future results.

None of the contents should be considered as advice or a recommendation to investors or potential investors in relation to holding, purchasing or selling securities or other financial products or instruments and does not take into account your particular investment objectives, financial situation or needs. Before acting on any information you should consider the appropriateness of the information having regard to these matters, any relevant offer document and in particular, you should seek independent financial and legal advice. Statements of opinion and recommendation will be introduced as such and generally reflect to judgement or opinion of Karl Rogers. These opinions may change at any time without written notice and ACE Capital Investments assumes no responsibility to send updates regarding any changes.

This document may not be reproduced in whole or in part, and may not be delivered to any person without the prior written consent of the author.

Any references to product(s) offered by ACE Capital Investments is not an offer to sell, or a solicitation of an offer to buy, a partnership interest in any fund described herein. No such offer or solicitation will be made prior to the delivery of the applicable offering memorandum and other materials relating to the matters mentioned herein. No representation or warranty is made by any fund or any other person (including any of its agents or other representatives) as to the accuracy or completeness of the information contained herein. Only those particular representations and warranties which may be made in definitive agreements relating to the funds, when, as and if executed, and subject to such limitations and restrictions as may be specified in such definitive agreements, shall have any legal effect.

The information contained herein was taken from financial sources that were deemed to be reliable and accurate at the time of publication. Changes in the market may cause this information to become out-dated or obsolete.

Neither Karl Rogers or ACE Capital Investments are affiliated with, or endorse, sponsor, or recommend any product or service advertised herein, unless otherwise noted.

***

The views expressed in this article are those of the author and do not necessarily reflect the views of AlphaWeek or its publisher, The Sortino Group

© The Sortino Group Ltd

All Rights Reserved. No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or scanning or otherwise, except under the terms of the Copyright, Designs and Patents Act 1988 or under the terms of a licence issued by the Copyright Licensing Agency or other Reprographic Rights Organisation, without the written permission of the publisher. For more information about reprints from AlphaWeek, click here.