Continue To Allocate to Private Equity but Be Selective

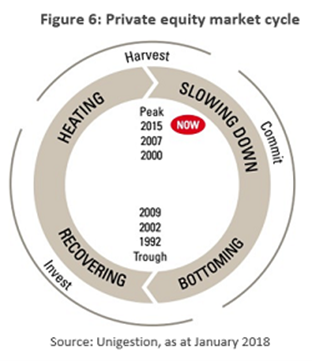

Private equity valuations have nearly reached the highs seen before the financial crisis and, due to slowing investment activity, seem to have peaked and stabilised during the second half of 2017, at least in North America and the Asia Pacific region.

Investor appetite for the asset class nonetheless remains strong. Competition at auction is fierce as private equity sponsors seek to redeploy record levels of committed capital. Given the need to compete on price, sponsors have been willing to put more leverage on their deals and we have seen a spike in average leverage levels in recent months, particularly at the large end of the market. However, leverage is apparently being used more responsibly than before as sponsors are structuring the debt to better reflect the nature of the business.

A positive outlook for private equity overall

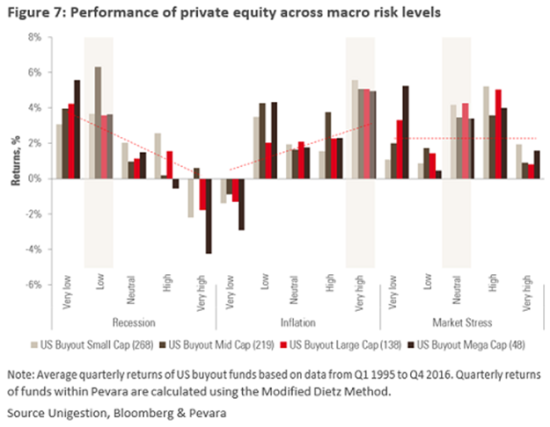

We expect returns from private equity to remain attractive in the years to come, both in absolute and relative terms. The economic background remains supportive overall, with continued growth likely to be positive for top-line company revenues. Private equity tends to perform well when the economy is growing and underperform during recessions, as shown in Figure 7.

Furthermore, as it becomes more difficult to make money in traditional markets such as equities and bonds, the illiquidity premium of private equity makes sense in an overall portfolio as a performance booster. Finally, as more and more companies are choosing not to list publicly, the private sector offers a set of interesting investment opportunities not available in the public market.

Be aware of correlation to equity and credit markets

That said, some caution is needed. High valuations in public equity markets could weigh on private equity. Correlation analysis shows that private equity does tend to move somewhat in line with public equity, albeit not in perfect synchronicity as it is less subject to market sentiment. It is interesting to note that buyouts tend to follow the S&P 500 and the MSCI World indices, while venture capital is more related to the NASDAQ.

Private equity, especially buyouts, also seem to move somewhat in sync with the high yield market, although with no correlation to the investment grade credit segment. This is because private equity needs leverage and capital-efficient structures to be able to generate the required return. In this current environment, where high yield is expensive, and we are entering a quantitative tempering phase, it will be important to avoid excessive leverage.

Focus on price discipline and be cautious on leverage

Private equity fundraising hit a new record in 2017, with some USD 453 billion raised over the year. As a consequence, finding good investment opportunities and maintaining price discipline in a competitive environment will be the biggest challenges for private equity investors in 2018. It will be important to invest in companies that can deliver the required base case return without relying solely on leverage and multiple arbitrage i.e. sector consolidation with synergies, powerful long-term trends and/or opportunistic market dislocations.

While we do not think that increasing debt levels should yet be a cause for concern, we continue to back private equity managers whose returns are driven by revenue growth and operational improvements rather than leverage. The average company debt multiples in our portfolios remain below 3x EBITDA. Cheap debt is a great way to optimise returns for investors, as long as it is used responsibly.

Given the level of competition, we prefer strategies that allow sourcing deals outside of large auctions. We therefore focus on small and mid-market buyouts or on sector-focused strategies. Smaller deals require deep local knowledge and strong operational capabilities. They are by nature less competitive than larger deals. In secondaries, the plain vanilla acquisitions of stakes in broadly known funds are mostly intermediated and too expensive. Thus, we favour secondary direct transactions, fund restructurings, as well as the acquisition of stakes in quality but smaller and less known funds.

If managed correctly, private equity can be a relatively defensive asset class. Investors can target sectors, especially in the small and mid-market, which are less correlated to GDP growth, such as education, healthcare, software or renewable energy. Furthermore, while private company valuations may fall during a slowdown, the declines are usually not as dramatic as in the public markets. Private equity managers have the luxury of time: they do not need to sell in adverse markets but can hold on to their portfolio companies until conditions improve.

**********

Fiona Frick is CEO of Unigestion

***

The views expressed in this article are those of the author and do not necessarily reflect the views of AlphaWeek or its publisher, The Sortino Group

© The Sortino Group Ltd

All Rights Reserved. No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or scanning or otherwise, except under the terms of the Copyright, Designs and Patents Act 1988 or under the terms of a licence issued by the Copyright Licensing Agency or other Reprographic Rights Organisation, without the written permission of the publisher. For more information about reprints from AlphaWeek, click here.