Court In Session: The People (VIX) Vs. Bonds

While our attention may be tempted to focus, in the near term, on potentially forthcoming Supreme Court cases dealing with the election, the most important case for investors to adjudicate has nothing to do with politics or policy. At this point, the greatest challenge for institutions and investors alike no longer even has to do with future Fed policy. The most important issue in two generations is derived from a simple reality—a 30-year treasury bond that now yields less than 2% annually and a 10-year treasury note that yields less than 1% annually.

According to Ibboston SBBI data, during the falling interest rate environment (favorable for bond prices) from 1980 to 2020, long-term treasury bonds returned investors between 9-10% annually. For comparison, the rising rate environment (not favorable for bond prices) from 1940 to 1980 resulted in an estimated 2-3% return annually for long-term treasury bonds. For long term bonds to achieve even something remotely close to 9-10% annually over the next 40 years, long term interest rates would need to fall into significant, uncharted, negative territory. Therefore, the returns in long term treasury bonds will not likely repeat the results of the last 40 years. It is time to find a new solution.

Investors who argue the point that yield is not the key reason to invest in bonds—that it is the flight-to-quality-protection during equity stress and crisis—we agree with the premise. But only so far. It is true that long term treasury bonds have rallied when overall equity prices have fallen. Treasury bonds have played an important counterpoint in investor portfolios in such periods. However, these counterbalancing, offsetting moves in long-term treasury bonds have returned a token result at best over the last 12 years. What is worse is the offsetting virtue of bonds over equities actually reverses beyond 5% pullbacks in equities. In other words, for negative equity months between 0 and -5%, the offsetting treasury bond return has been around +1-3%., or a 0.5:1 ratio. However, if equity markets fell beyond 5%, treasury bonds waned in the protection they provided. If equity markets fell -6%, investors could expect treasury bonds to deliver +4.5%. But if equity markets fell -10%, treasury bonds only demonstrated an expected return of +1.9%, or a 0.2:1 ratio. In fact, for negative equity moves beyond -5%, long-term bonds actually began to show positive correlation tendencies to the equities they are meant to counteract!

The impact of low interest rates has a circular affect as it pertains to risk and portfolio protection. Thanks to these low bond yields, investors are now faced with a difficult reality. The need for higher yield has pushed investors to seek more risk. Often, that risk takes on a different form of equity risk. Whether that risk is structured in private credit, real estate, corporate bonds, or dividend yielding equities—equity risk prevails. This uniform risk profile makes investors one-dimensional. Hence, we now live in a light-switch world of “risk-on / risk-off.” Investors now live in a world-psyche that either compels them to pursue equity risk (risk-on) or, at the flip of a switch, flee from it (risk-off). If investors believe treasury bonds will support their now overly-equity-risk-heavy portfolios when the “risk-off” lights go out, they may likely find out that is not the case. And as we have discussed above, the darker the “risk-off” night, the less likely the treasury bond flashlight will shine brightly enough to light the way forward. Treasury bonds have a decreasing effect the harder equity markets fall, thus making it almost impossible to cushion an equity-risk-heavy portfolio—which is the unfortunate status of many investors today.

You may therefore delight to know an instrument exists which has historically fully matched past equity market drawdowns on a consistent basis and, through active management, offers a potential form of return during non-crisis periods—VIX Futures. In other words, VIX Futures offers the opportunity to fulfill negative correlation, convexity requirements as well as non-crisis return potential—thus absolving institutional need to pursue the bottom of the yield barrel or take on additional and potentially perilous forms of equity risk. VIX Futures is the instrument that, in our opinion, is the best solution to protect investors from “risk-off” disruptions.

In this case, we will present clear empirical evidence that VIX Futures should replace long-term bonds in institutional portfolios. Welcome to The People (VIX) vs. Bonds.

Bonds

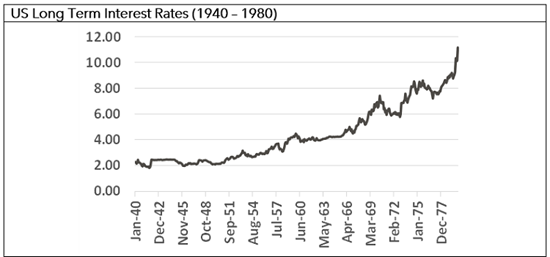

The below chart shows the rising long-term interest rate environment from 1940 to 1980. Suppressed by rising rates, bonds struggled to eek out a positive 2-3% annual return during this period.

US Long Term Interest Rates (1940 – 1980)

Source: Ibbotson data, CFA Institute

However, fortunes changed for long-term treasury bonds in 1980. With declining inflation and a more accommodative Fed, interest rates have declined precipitously over the last 40 years. To be sure, long term treasury bonds have rewarded investors with 9-10% annual returns during that stretch.

30-Yr Constant Maturity Rate (1980-2020)

Source: St. Louis Federal Reserve

Now that interest rates have declined near the zero-level, and unless long term interest rates move into significantly negative territory, investors can hardly expect to achieve such terrific returns from long-term treasury bonds over the next forty years. Investors are looking for yield solutions. Many practitioners have advocated solutions with severely perilous ramifications: real estate, private credit, corporate bonds…As if these substitutes are driven by different underlying factors than what drive the equity markets themselves! Indeed, they may offer yield. But they do not provide that classic counterbalancing role long term treasury bonds have fulfilled historically. Implicitly, by suggesting alternative yield, these practitioners who have put these ideas forward are admitting the opportunity in long term rates has waned. Bonds simply can’t continue to deliver their historical returns of the last 40 years going forward.

With the yield question conceded, what of that counterbalancing role bonds have played?

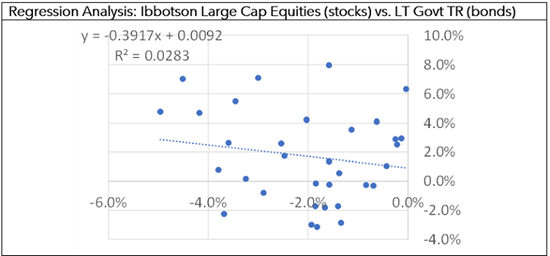

From November 2007 to September 2020, Ibbotson Large Cap Equities have returned negative results in 51 of 155 months. Of those 51 negative months, 33 have ranged between 0 to -5%, with a median return of -1.8%. Counterbalancing those equity market declines, long-term treasury bonds have returned a median 1.4% in those same months. The scatterplot of those 33 monthly periods is shown below.

Regression Analysis: Ibbotson Large Cap Equities (stocks) vs. LT Govt TR (bonds)

Source: Ibbotson Data, CFA Institute

As seen above, long-term treasury bonds have exhibited a solid negative correlation

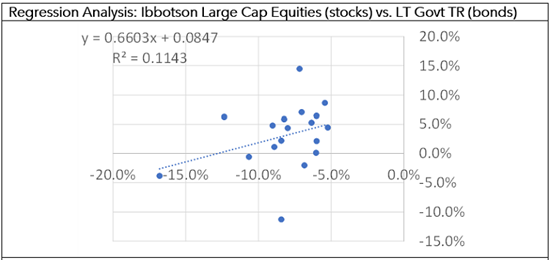

(-0.17) to equities when equity monthly drawdowns have not exceeded -5%. However, in the remaining 18 months when monthly equity drawdowns exceeded -5%, long term treasury bonds behaved quite differently. Long-term treasury bonds actually turned to a positive correlation (0.34) with equities and exhibited a declining counterbalancing effect. The median return for long-term treasury bonds for this segment of the data was 4.4% while the median monthly decline for equities was -7.6%.

Regression Analysis: Ibbotson Large Cap Equities (stocks) vs. LT Govt TR (bonds)

Source: Ibbotson Data, CFA Institute

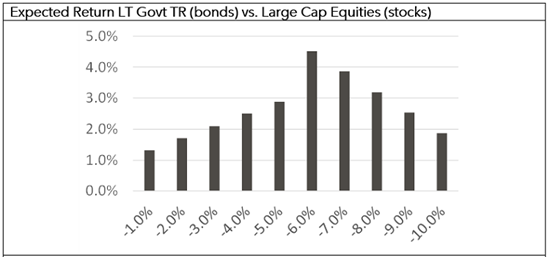

When we break the Large Cap Equity data into those two segments of negative returns (0 to -5% and <-5%), we can perform a least squares regression on the two data sets. Using the regression equation, we can determine an expected return on long-term treasury bonds for every 1% decline in monthly equity returns.

Expected Return LT Govt TR (bonds) vs. Large Cap Equities (stocks)

Source: Ibbotson Data, CFA Institute

Even when outliers are removed, long-term treasury bonds change from exhibiting positive convexity (increasing protection against equity markets) to negative convexity (decreasing protection against equity markets). In other words, the worse the drawdowns become in equity markets, the less effective long-term treasury bonds become in delivering a counterbalancing offset. To be sure, the expected return in long-term treasury bonds is +1.9% for a -10% decline in Large Cap Equities.

Therefore, given bonds have exhausted the declining interest rate tail-wind of the last 40 years and that their counterbalancing properties do not show the quality or consistency of offset required to stabilize an equity-heavy portfolio, we assert the use of long-term bonds in a portfolio is over.

VIX Futures

On the other hand, VIX Futures has exhibited greater coverage of equity market drawdowns overall, but more importantly, a progressively higher positive convexity to larger equity market drawdowns.

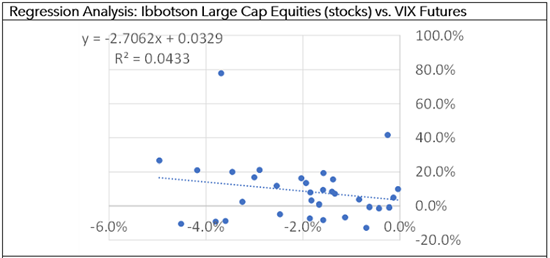

We again segment the 51 negative equity months into the 33 months where equities had drawdowns between 0 and -5% and the 18 months with equity market drawdowns over -5%.

The scatterplot of the first data segment show a strong negative correlation and convexity. In reality, the VIX Futures returned a median 7.2% compared to equities (recall the median equity return of -1.8% from above). The correlation between the two return sets is -0.21.

Regression Analysis: Ibbotson Large Cap Equities (stocks) vs. VIX Futures

Source: Ibbotson Data, CFA Institute, CBOE

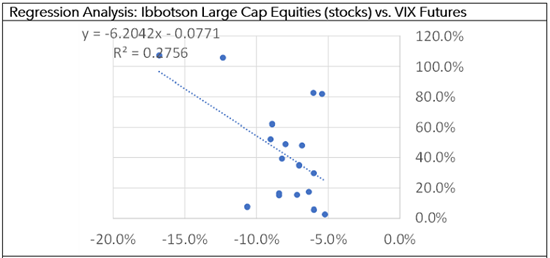

The scatterplot of the second data segment shows an accelerating negative correlation and increasing convexity. In months when equities returned less than -5% (-7.6% median), VIX Futures returned an astounding median 37.1%. The correlation between the two return sets intensified to -0.52.

Regression Analysis: Ibbotson Large Cap Equities (stocks) vs. VIX Futures

Source: Ibbotson Data, CFA Institute, CBOE

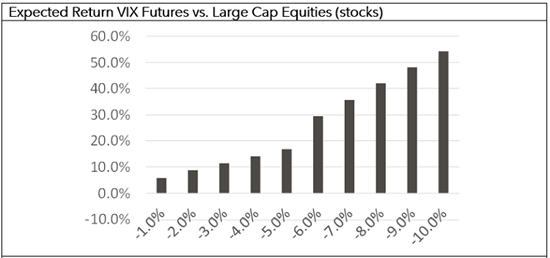

Again, if we derive the least-squares regression equation and use it to calculate an expected return for VIX Futures, we find VIX Futures exhibits a higher positive expectancy the larger the monthly equity drawdown—exactly what one would want in an ideal counterbalancing instrument.

Expected Return VIX Futures vs. Large Cap Equities (stocks)

Source: Ibbotson Data, CFA Institute, CBOE

Conclusion

VIX Futures tops long-term treasury bonds both in terms of magnitude of coverage and growing convexity with respect to negative monthly drawdowns in equity markets. Empirically, this claim is irrefutable. Therefore, institutions should look to actively managed programs which harness VIX Futures as potential resources for bond replacement solutions to cushion the blow when the risk-off lights go out on their now equity heavy portfolios.

This court finds bonds guilty as charged.

**********

Timothy R. Jacobson, CFA is a Managing Partner at Pearl Capital Advisors

Lawson E. Stringer is a Managing Partner at Pearl Capital Advisors

***

The views expressed in this article are those of the author and do not necessarily reflect the views of AlphaWeek or its publisher, The Sortino Group

© The Sortino Group Ltd

All Rights Reserved. No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or scanning or otherwise, except under the terms of the Copyright, Designs and Patents Act 1988 or under the terms of a licence issued by the Copyright Licensing Agency or other Reprographic Rights Organisation, without the written permission of the publisher. For more information about reprints from AlphaWeek, click here.