Crash or Consolidation: The Next Phase in Equity Markets

Earnings drive markets. In the long-run, no other factor plays a larger role in determining public-equity returns. By how much and at what rate companies can grow earnings determines long-term stock market performance. Below we will present two long-term data sets which support the thesis that institutions should consider altering their exposures to equities over the next 10-20 years, regardless if the path to lower equity returns comes via a crash or a long-term consolidation.

Corporate Earnings: St. Louis Fed Data

The St. Louis Fed and the Bureau of Economic Activity (“BEA”) publish data on corporate earnings growth dating back to 1947:

- Corporate Profits After Tax with Inventory Valuation Adjustment (IVA) and Capital Consumption Adjustment (CCAdj) (“CPATAX”)

- Corporate Profits After Tax (without IVA and CCAdj) (“CP”)

In this paper, we will not debate the rationale for making these adjustments. Nevertheless, the BEA offers the following explanation regarding the IVA and CCAdj adjustments:

“This measure [CPATAX]–profits from current production–is the income that arises from current production, measured before income taxes, of organizations treated as corporations in the national income and product accounts (NIPAS). With several differences, this income is measured as receipts less expenses as defined in Federal tax law. Among these differences are: Receipts exclude capital gains and dividends received; expenses exclude bad debt, depletion, and capital losses; inventory withdrawals are valued at current cost; and depreciation is on a consistent accounting basis and valued at current replacement cost.”

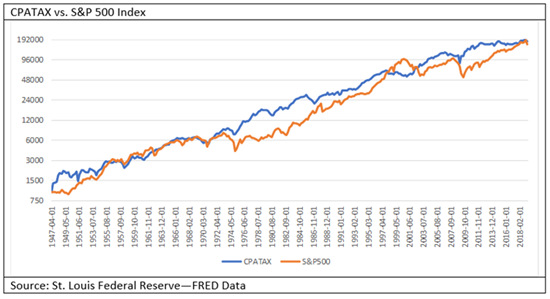

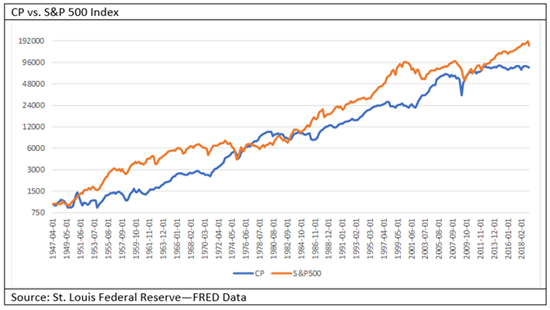

If we compare the relationship of CPATAX and CP to the S&P 500 we can observe a strong correlation between corporate earnings and the value of the S&P 500. To begin, we baseline both the earnings and the S&P 500 data with a starting value of 1000 and compounding the growth going forward.

At first glance, the two charts seem to show diverging stories about the valuation of equity markets. In observing the CPATAX chart, one might conclude equity markets are currently properly valued and in-line with adjusted corporate profits. However, when we examine the unadjusted earnings CP chart, we see a noticeable and concerning divergence that has formed over the last several years.

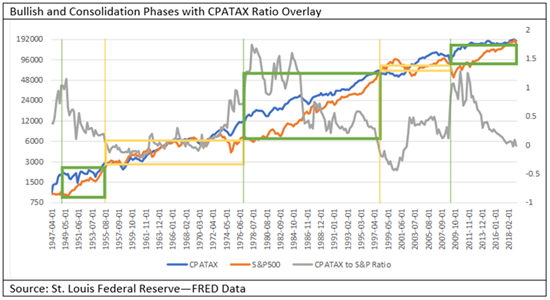

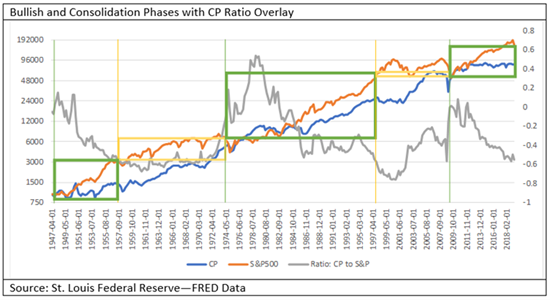

To move beyond this first-order comparison of tracking the compounded growth of corporate earnings against the S&P 500 and to discover the true trajectory of corporate earnings, it may be helpful to create a ratio between each data set and the S&P 500. The following exercise may also inform us of our current standing within the earnings cycle.

Using the baselined indices, the respective ratio formulas are (CPATAX / S&P 500) -1 and (CP / S&P 500) -1. Effectively, these two ratios signal long-term, cyclical shifts between moments when the growth of corporate earnings outpace the growth in the S&P 500 and visa versa. Although the timing of these signals is not perfectly synchronized, the two do capture the same general areas of market expansion (bull trend) or market consolidation. The signals are created using the following rules:

- When (CPATAX / S&P 500) -1 reaches a value of 0, a bullish trend is initiated. When the value reaches 0, the consolidation phase begins. As the value returns to 1.0, a new bullish trend resumes.

- When (CP / S&P 500) -1 reaches a value of 0, a bullish trend is initiated. When the value reaches negative -0.6, the consolidation phase begins. As the value returns to 0, a new bullish trend resumes.

The following charts show these cycles and their coincidence with the bull trend (green outline boxes) and consolidation (yellow outline boxes) phases in the S&P 500.

At our current juncture in the earnings and market cycle, we are at or nearing the two levels that would usher in a new consolidation phase. Historically, these consolidation phases have lasted 10-20 years and offer muted to even potentially negative IRRs in the S&P 500. During the first consolidation period shown between roughly 1955 and 1975, the S&P 500 returned approximately 3-6% annually. These returns compare unfavorably with our current bull trend which has produced IRRs around 8-10%.

CAPE Ratios Data

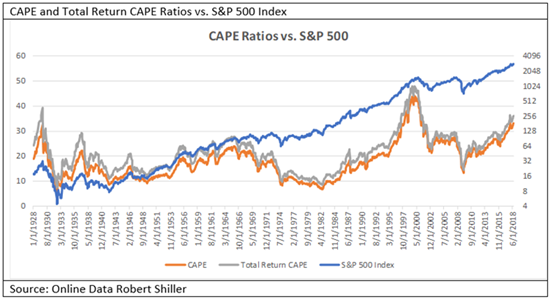

Another set of supporting data to the long-term thesis presented above are the CAPE (cyclically adjusted price-to-earnings) Ratios pioneered by Robert Shiller. In his book, Irrational Exuberance, Shiller presents his form of the classic price-to-earnings ratio by smoothing the earnings over a 10-year average and adjusting those earnings for inflation. In 2018, Shiller produced an alternative CAPE ratio, called the Total Return CAPE, which also makes adjustments for corporate buybacks or share repurchases. Below, we can see these ratios plotted against the S&P 500 since 1928.

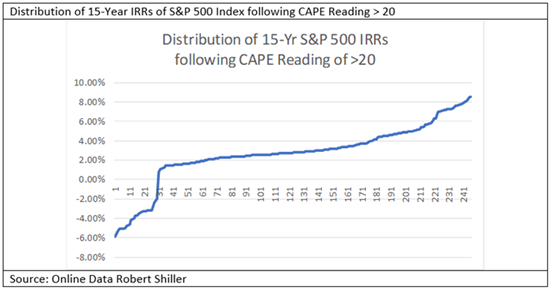

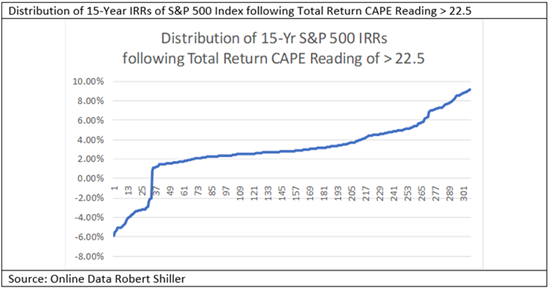

Optically, one can observe that readings of CAPE Ratios above 20 correspond with markets which perform below average for a period of time. To be sure, below we present the 15-year returns, or IRRs, of the S&P 500 following quarterly readings of a CAPE Ratio greater than 20 (246 periods) and a Total Return CAPE Ratio of greater than 22.5 (307 periods). As we can observe, the following 15 years do indeed deliver below average returns.

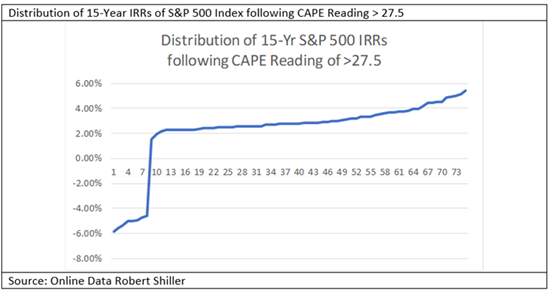

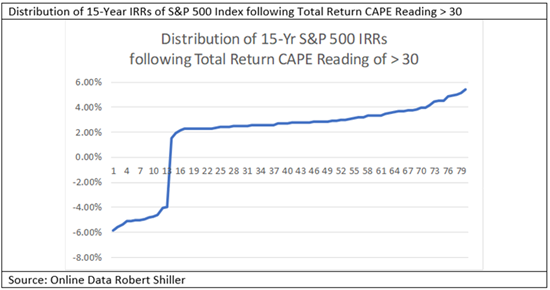

We also present the same analysis for CAPE (75 periods) and Total Return CAPE (80 periods) readings above 27.5 and 30, respectively.

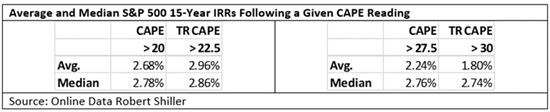

The 15-Year average and median IRRs following readings of the levels described above are also shown below:

Average and Median S&P 500 15-Year IRRs Following a Given CAPE Reading

Recently, both CAPE Ratios have registered and maintained levels above 30, suggesting the next 10-20 years are likely to deliver below average IRRs in the S&P 500. The only other times these ratios have sustained levels above 30 since 1928 include just before the Great Depression and the dotcom bubble. This time could be different, but the weight of the evidence supports lower IRRs. Institutions that disregard this data should not do so lightly.

Conclusion

While investors may primarily fear and make preparations for a severe sell-off which can happen during these periods of consolidation, investors should not neglect preparations for a potential period of stagnant, sideways markets as the actual path we may experience as the earnings / market cycle resets.

Over the near- to medium-term horizon, markets may experience significant advances which may give pause to the overall thesis presented here. After all, nothing about the cyclical levels described herein means they can’t or won’t become more extended. However, we feel it is clear that the current earnings / market cycle is stretched and will look to reset over a significant period of time as has occurred historically.

Furthermore, regardless of whether the reset assumes a crisis crash, a frustrating stagnation or an advance with a consolidation, it is our view that institutions may need to make portfolio adjustments for a potentially significant period of low equity returns. Institutions should consider favoring investments and strategies which offer yield and steady cash flows and/or rely on low-correlation, relative-value and alternative betas which offer growth-like returns but which are not reliant on the same systemic factors as equity markets.

**********

Timothy R. Jacobson, CFA is a Managing Partner at Pearl Capital Advisors

Lawson E. Stringer is a Managing Partner at Pearl Capital Advisors

This presentation is for informational purposes only. These results of the Pearl Hedged VIX program (“Program”) are compiled by Pearl Capital Advisors, LLC and are unaudited and may be incomplete or even inaccurate, although are deemed to be generally reliable. None of the results or analysis included herein should be construed as an offer to sell. Investors should consult their own adviser, legal, and tax consultants before making any investment decision. Individual accounts may vary in performance depending on size, funding level, and fee structure.

***

The views expressed in this article are those of the author and do not necessarily reflect the views of AlphaWeek or its publisher, The Sortino Group

© The Sortino Group Ltd

All Rights Reserved. No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or scanning or otherwise, except under the terms of the Copyright, Designs and Patents Act 1988 or under the terms of a licence issued by the Copyright Licensing Agency or other Reprographic Rights Organisation, without the written permission of the publisher. For more information about reprints from AlphaWeek, click here.