A Fall To Forget and a December To Remember?

As the summer drew to a close, allocators to hedge funds finally seemed in relative agreement that the environment had improved and they were again picking their heads up, no longer toiling in obscurity. The ingredients for which active managers were yearning were finally available in the market. There was dispersion amongst assets, strategies, and managers. The passive crowd had not achieved the returns promised for a variety of reasons. Volatility had returned to equity markets and also seemed to be episodically showing up in other assets. The Fall of 2018 was setting up for hedge funds to put up solid numbers and thus reclaim their higher fee throne. Some advisers, like Sussex, had been advocating for inclusion of strategies non-correlated to equity market direction, or even protective in a sustained sideways or down market to complement the return of active management.

October has often been a troubling month, but the meltdown of equities apparently came as a surprise to many hedge fund managers. While some had been ruminating about the end to the equity market euphoria and still others had begun to prepare for the end of the bull market rally via adding uncorrelated, protective assets to the portfolio, there ended up being almost no place to hide. As happens in a risk-off scenario, the market turn started out disguised as idiosyncratic events but quickly spread, with correlations increasing daily. Fast forward to November/early December and the damage has spread despite periodic relief rallies which have only served to blindside traders and perhaps encourage perma-bulls.

The allocators and advisers that had been attempting to shift portfolios into a more protective stance fared better, but generally did not produce a positive return. So the December question that will fill conference rooms is, 'What now?' If one was in the camp of adding strategies that are non-correlated to the major markets (equities, interest rates, and credit spreads) then the decision is whether to stay the course into year-end and beyond. The most cited non-correlated strategy is probably Trend Following and the sharp moves in the equity market wreaked havoc with most of these systems fostering concern. On cue, the fickle pundits have once again begun to point to systematic strategies as the cause, or at least the accelerant, to market downturns.

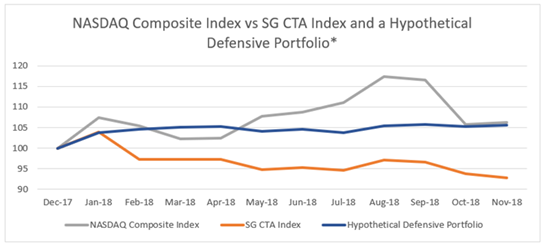

* Hypothetical Defensive Portfolio performance is representative based on pro-forma returns for a portfolio of hedge funds constructed by Sussex Partners to protect against market drawdowns

At Sussex, we have long-favoured newer technology trend systems that include more thoughtful entry/exit points and risk control, in some cases utilising AI to dynamically alter the models. Even given that those programs fared better in October and November, they did not serve to protect (i.e. produce gains) the broader portfolios as intended. The culprit in October and November for priced-based systems (trend and beyond) was, not surprisingly, equity exposure. Depending upon the day, strategies took losses on both the long and short side, in many cases getting whipsawed with the market’s gyrations. Interestingly as the volatility and volatility of volatility picked up, so did losses.

The market gyrations of the Fall have been assigned multiple causes in addition to the ‘momentum’ traders, but to those being buffeted it almost does not matter if this, trade, Brexit, etc. are to blame. It is now even more clear that investors need to take action leading into 2019 to move some portion of their traditional or alternatives exposure into non-correlated protective strategies. The immediate learning is to try and limit the equity exposure within this basket as getting the direction correct is quite difficult in the short term.

Moving Forward

While some cathartic lessons can be extracted from portfolio analysis, the path of global markets is less clear and is likely to be resolved in a more volatile fashion. It is here that a forward-looking view, informed by experience, needs to hold sway. The view is quite simple, markets are finally again on the move. Whether it be global equities, credit spreads, rates, or commodities there is increasing dispersion, directionality, and more normal levels of volatility. The first sign of a change in the investment environment was perhaps among heavily held equities, but increasingly there are differing opinions reflected in prices across markets. A carefully constructed, thoughtfully diversified basket of non-correlated strategies will work. In fact, it did work during the latest tempest when measured against most metrics other than absolute return. A holiday goal should be a tweak of the positions to focus on those which should have less equity directional exposure (which we believe will remain problematic), and to increase exposure to those strategies that have proven adaptable to what is going to become a significantly less bullish environment. With these changes, a December to Remember might yet be in the offing.

**********

Jim Neumann is Partner and Chief Investment Officer at Sussex Partners

***

The views expressed in this article are those of the author and do not necessarily reflect the views of AlphaWeek or its publisher, The Sortino Group

© The Sortino Group Ltd

All Rights Reserved. No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or scanning or otherwise, except under the terms of the Copyright, Designs and Patents Act 1988 or under the terms of a licence issued by the Copyright Licensing Agency or other Reprographic Rights Organisation, without the written permission of the publisher. For more information about reprints from AlphaWeek, click here.