Integrated Alpha: The Future of ESG Investing

PanAgora has a long history of innovative alpha factor development. Our investment philosophy is rooted in quantifying the fundamental drivers of company performance. Our current suite of factors not only identify companies that have dominant competitive advantage within their industry, but also ones which take into consideration their shareholders, employees, and customers best interests as well as the environment, when devising their corporate mission.

For over a decade we have been identifying management decisions that have an impact on a company’s valuation. After interviewing forensic accountants who manually go through thousands of pages of company filings to find signals of potential earnings manipulation, we developed a quantitative process to identify the same red flags over a much broader universe of companies more quickly. In the process, PanAgora has become the second heaviest user of EDGAR, the SEC’s document service 11.

During hundreds of discussions with career sell-side analysts and management consultants, we synthesized the age-old challenge of evaluating the skill of executive management teams into a list of quantifiable criteria. The companies the algorithm chooses are the top based on minimizing the agency conflict between shareholder rights and personal executive gain. They also have independent board members who ensure the highest level of corporate governance and oversight.

The firms we invest in also typically have motivated employees. We don’t want to simply take the management’s word on the morale of their employees, which is why we employ web-scraping techniques to “read” millions of direct comments from employees on their thoughts of management, how likely they are to recommend their company to a friend, and their overall job satisfaction. We want to invest in companies which recognise the importance of employee happiness on their success.

Management behaviour insights are also used to develop ESG alpha factors. As an example, there is a common behavioural tendency for C-Suite executives to avoid disclosing negative news too early 12. As a result of this behavioural tendency, we verified that upon disclosure of negative ESG news, companies tend to work to remedy their ESG related issue, and this results in improved ESG alpha. Furthermore, the act of disclosing ESG related issues indicates that ESG is important to a firm’s management. Constructing this ESG alpha factor entails developing a proprietary ESG dictionary, reading through millions of companies’ internal corpus to identify and assign relevant ESG information using natural language processing (NLP) techniques, and then applying machine learning techniques to assess the relative impact of ESG comments.

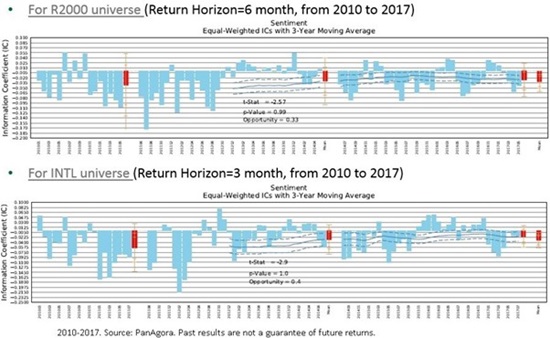

The charts below show the alpha performance of this factor in the US and International universes, constructed around Russell 2000 and MSCI World ex. US indices, respectively, and described in disclosures. Signs are flipped because disclosing negative ESG news is positive for ESG alpha, and vice versa.

As a final example of ESG alpha factors in our library, we utilize the wisdom of informed investors. Many studies have documented that stocks commonly held by institutional investors have better alpha performance over time 13. The same conclusion can be drawn for stocks held by ESG funds with respect to ESG ratings, and subsequently alpha through economic channels mentioned above. Below is the alpha performance for this factor in the US.

PanAgora’s ESG Factor Materiality Categorization

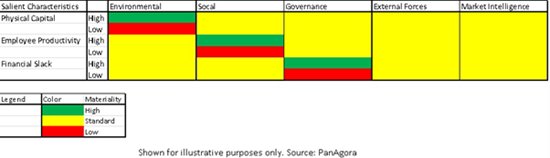

Materiality of ESG factors varies across companies. Environmental issues are important to industrial companies, and not as important to professional service companies, while employee satisfaction is important to professional service companies and not as important to companies whose assets are mostly physical-capital-based. The common approach to identifying materiality is to segment companies by industry. However, we believe this is not the most ideal method to measure materiality.

PanAgora utilizes Contextual Modeling, as documented in a 2005 14 paper, which identifies the power of factors such as value, quality, and momentum has different efficacy across various risk contexts. In recent years, PanAgora has applied a similar approach across its suite of ESG alpha factors, not along risk dimensions as in [QHS, 2007] but rather depending on salient firm characteristics, to evaluate materiality of ESG alpha factors and determine which ESG alpha factors are most relevant to each company. This process cuts through industry group and can identify differences across companies within an industry. For example, Netflix and Yum! Brands are both in the consumer discretionary sector however we believe relevant ESG alpha (and standard alpha) factors are different for the two companies. The below graph shows examples of ESG alpha factor materiality through this approach.

PanAgora’s Integrated ESG Portfolio Construction

We believe investors generally focus on maximizing alpha generation while minimizing downside risk. ESG-minded investors face additional decisions we believe may be equally important:

How important is ESG exposure versus alpha? For example, is the asset owner willing to give up some expected alpha in order to improve her portfolio’s ESG rating by a certain percentage?

Which ESG metrics matter? That is, while carbon footprint may be a priority for certain SWF, workplace equality could be the most important ESG issue for a local government employee pension fund.

The answer will differ between asset owners and even when this is known the challenge still remains in constructing an ESG portfolio with the objective of maximizing along two dimensions: ESG and Alpha. In addition to innovative, proprietary ESG alpha factors and evaluating the materiality of these factors via a novel approach, PanAgora has also developed an Integrated ESG Modeling Framework. We believe this framework addresses the above concerns of asset owners by constructing a bespoke portfolio, which holistically integrates standard and ESG alpha factors in a manner that seeks to satisfy the dual objectives of maximizing alpha and ESG performance.

The Integrated ESG Modeling Framework has the following characteristics:

• Flexible: The Framework has the ability to adjust standard and ESG alpha levers based on asset owner preferences or investment policy requirements. The framework is agnostic to the relative importance an asset owner assigns between ESG and alpha performance.

• Relevant: The Framework takes in any ESG metric the asset owner cares about. Since it is agnostic to the ESG measure selected, each asset owner may select the particular ESG metric that matters to her.

• Dynamic: As alpha and ESG performance of the various standard and ESG alpha factors ebb and flow, the model dynamically adjusts factor weights in an effort to optimize alpha generation and ESG performance.

PanAgora’s ESG Portfolio Measurement and Reporting

We believe measurement and reporting are critical components to assessing the impact of ESG measures within portfolios. As a quantitative firm, PanAgora provides portfolio attribution reports by utilizing in-house tools to assess alpha and external vendor ESG data to strive for consistency with broad-based metrics when evaluating ESG characteristics and measuring performance. Examples of ESG measures and reports that can be provided to asset owners include, but are not limited to, the following:

- Overall portfolio ESG rating.

- Carbon exposure.

- Alignment of portfolio companies with SDGs to access real world impact.

In addition, in-depth reporting of various companies owned in the portfolio is also possible. We believe the choice of using independent, third party ESG measurement providers offers unbiased results.

Conclusion

As the world becomes increasingly ESG-minded and a new generation of investors begins to drive change in the investment world, we will see more ESG strategies come to market. We believe one of the challenges for investors is the lack of a broadly accepted definition or guideline for constructing ESG portfolios. There are however certain networks, such as the United Nations Principles for Responsible Investment (UN PRI), that help to define and hold members accountable for such practices. As a signatory of the UN PRI, we have utilized these guidelines to develop our ESG framework.

As a result, PanAgora has created a library of ESG alpha factors, evaluating materiality of factors through contextualization technology, and an integrated ESG portfolio construction framework, that we believe is flexible, relevant and dynamic. ESG is a rapidly evolving investment field with myriad definitions, and no well-defined process to construct a portfolio.

At PanAgora, as described above, we believe an ESG portfolio can be constructed using our framework in a manner that seeks to meet both the return objectives and values of the asset owner.

**********

George Mussali is CIO and Head of Research at PanAgora Asset Management

Mike Chen is Portfolio Manager at PanAgora Asset Management

This article is an abridged version of ‘Integrated Alpha: The Future of ESG Investing’ which is available for download on PanAgora’s website

***

The views expressed in this article are those of the author and do not necessarily reflect the views of AlphaWeek or its publisher, The Sortino Group

© The Sortino Group Ltd

All Rights Reserved. No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or scanning or otherwise, except under the terms of the Copyright, Designs and Patents Act 1988 or under the terms of a licence issued by the Copyright Licensing Agency or other Reprographic Rights Organisation, without the written permission of the publisher. For more information about reprints from AlphaWeek, click here.