Kettera Strategies Heat Map - September 2023

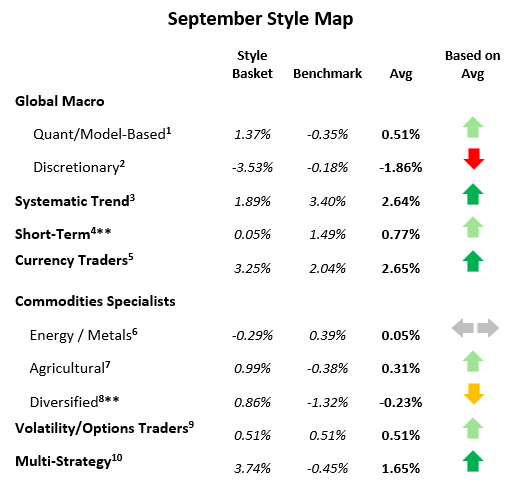

Systematic Trend Strategies

Long-term trend followers had a nicely positive month, driven by a few rather strong trends. The best performing sector for most strategies was fixed income and rates, where most programs were short and caught the rise in yields (bonds down), especially on the longer end. Long USD vs. most G10 and emerging market currencies, especially against shorts in Japanese Yen, Euro, and British Pound was also good positioning. Long the energy complex, namely crude (WTI, Brent), heating oil and gasoline was the third notable profitable trend. Equity indices was a notable loser across programs as long exposures were punished. It seems that the longer-duration systems, with holding periods months to years, slightly outperformed medium and shorter-term programs in September.

Discretionary Global Macro Strategies

Programs with longer-term horizons tended to perform poorly while programs with either short holding periods overall, or trade opportunistically around a theme, performed better. The longer-term, discretionary strategies were long fixed income and rates in anticipation of G10 central banks cutting sooner than later, and were punished as yields shot up. These same programs also bought dips in equities in a related theme, and hit as equities declined. The more successful programs appeared to be those trading opportunistically – e.g. short precious and base metals, short grains, and catching the strengthening US Dollar vs majors.

Quant Macro Strategies

Quant Macro strategies were positive in September, catching some of the same moves that the long-term trend programs caught, namely profits being short fixed income and rates, and long US Dollar vs. G10 currencies. Those quant programs that were long the energy complex also fared well. One notable difference vs their discretionary brethren was that the quants seem to have navigated equities better, catching the drop later in the month. Most programs struggled in metals, losing on long precious and base metal exposures.

FX Specialists

The currency markets in September were dominated by a strengthening US Dollar vs. most G10 (ex Sweden) and vs emerging market (commodity) currencies (ex Mexico). The USD strengthened primarily due to superior US economic data and higher real yields with a hawkish Fed. Systematic, fundamentally-based (econometric) programs performed well, using input from the interest rate markets to position themselves long USD, especially vs. the Japanese Yen and European currencies. Discretionary managers followed the same cues. Systematic, price-based programs, however, underperformed versus their fundamental peers, largely due to exaggerated short-term moves and intra-day price reversals hindering the capability to hold onto gains, with most programs ending the month flat.

Commodities Specialists - Agricultural Strategies

Most of the programs we follow in the grain and livestock sector were positive last month. There were quite a few programs that were down slightly, with a few more profitable programs that pulling overall sector (on average) in to positive territory. Discretionary traders dominate this sector, and most use a combination of outright directional trades and spreads (calendar and intra-commodity, e.g. corn v. wheat), often with long options strategies to limit downside. Relative value trading (spreads) seems to have underperformed as there wasn’t much volatility or movement until the last few days of the month. Most programs focused most heavily on the corn market, which traded in a tight range throughout. Programs that were successful were short wheat and the soybean complex using outright directional exposures. Returns in livestock positions was minimal last month as cattle (live, feeder, beef) traded in tight ranges.

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. See notes at end of this document for details on the construction of the Hydra "baskets" and the benchmark used for each style class. Also note that some baskets may contain managers that have not yet reported by this date. *=Less than 75% reported. **=Less than 75% reported and absence of a core manager's return.

*********

Footnotes:

For the “style classes” and “baskets” presented in this letter: The “style baskets” referenced above were created by Kettera for research purposes to track the category and are classifications drawn by Kettera Strategies in their review of programs on and for the Hydra Platform. The arrows represent the style basket’s overall performance for the month (e.g. the sideways arrow indicates that the basket was largely flat overall, a solid red down arrow indicates the basket (on average) was largely negative compared to most months, etc.). The “style basket” for a class is created from monthly returns (net of fees) of programs that are either: programs currently or formerly on Hydra; or under review with an expectation of being added to Hydra. The weighting of a program in a basket depends upon into which of these three groups the program falls. Style baskets are not investible products or index products being offered to investors. They are meant purely for analysis and comparison purposes. These also were not created to stimulate interest in any underlying or associated program. Nonetheless, as these research tools may be regarded to be “hypothetical” combinations of managers, hypothetical performance results have many inherent limitations, some of which are described below. no representation is being made that any product or account will achieve profits or losses similar to those shown. in fact, there are frequently sharp differences between hypothetical performance results and the actual results subsequently achieved by any particular trading program. one of the limitations of hypothetical results is that they are generally prepared with the benefit of hindsight. in addition, hypothetical trading does not involve financial risk, and no hypothetical trading record can completely account for the impact of financial risk in actual trading. there are numerous other factors related to the markets in general or to the implementation of any specific trading program which cannot be fully accounted for in the preparation of hypothetical performance results and all of which can adversely affect actual trading results..

Benchmark sources:

- Blend of Eurekahedge Macro Hedge Fund Index and BarclayHedge Global Macro Index

- The Eurekahedge Macro Index

- The Société Générale Trend CTA Index

- The Société Générale Short-term Traders Index

- The Barclay Hedge Currency Traders Index

- Blend of Bridge Alternatives Commodity Hedge Fund Index and Barclay Discretionary Traders Index (for February only the Barclay index was used as the Bridge index was unavailable.)

- The Barclay Agricultural Traders Index: (same link as above)

- The Eurekahedge Commodity Hedge Fund Index

- Blend of CBOE Eurekahedge Relative Value Volatility Hedge Fund Index and CBOE Eurekahedge Long Volatility Index (same link)

- Blend of Eurekahedge Multi Strategy Asset Weighted Index and Barclay Hedge Fund Multi Strategy Index

Indices and other financial benchmarks shown are provided for illustrative purposes only, are unmanaged, reflect reinvestment of income and dividends and do not reflect the impact of advisory fees. index data is reported as of date of publication and may be a month-to-date estimate if all underlying components have not yet reported. the index providers may update their reported performance from time to time. Kettera disclaims any obligation to verify these numbers or to update or revise the performance numbers.

***

The views expressed in this article are those of the author and do not necessarily reflect the views of AlphaWeek or its publisher, The Sortino Group

© The Sortino Group Ltd

All Rights Reserved. No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or scanning or otherwise, except under the terms of the Copyright, Designs and Patents Act 1988 or under the terms of a licence issued by the Copyright Licensing Agency or other Reprographic Rights Organisation, without the written permission of the publisher. For more information about reprints from AlphaWeek, click here.