Magnelibra 2019 Outlook

We have written exhaustively over the last decade in regards to the very simple game plan that the global central banks decided to embark upon. In 2008, with the initial passage of TARP and successive Quantitative Easing programs enacted by all the major central banks around the globe, the era of ZIRP commenced. This precipice, this singularity if you will, vaulted global economies out of the worst debt induced financial disaster since the Great Depression. Investors the world around cheered in joy as asset prices bottomed, and both equity and bond markets rose rapidly. A more astute observer of financial constructs, the Jim Grant, the David Rosenberg’s of the world, saw this as financial largesse at its finest as our central bank overlords swapped corporate and private defaulting debt, with AAA rated government debt in what would become the largest asset grab in history by global central banks.

As global central bank balance sheets ballooned, their coordinated efforts to keep short interest rates negative hit full steam ahead. In what looked to be a move straight out of the BOJ handbook, print money, buy assets and peg real rates negative. Who could possibly lose? Government coffers would be full of fresh debt to spend, leveraged Wall Street players would once again get the “all’s clear” to BUY, BUY, BUY! And that they certainly did, as the SP500 rose by factors, running from that all ominous low of 666 to a recent high of 2930, a 4.4x run. Who would have guessed?

The Federal Reserve’s balance sheet ran up from $900 billion to just over $4.5trillion, actually outpacing the factor gain of the SP500 as the Federal Reserves assets grew by a factor of 5x. What should be obvious to you, the reader, is that when central banks print, the money flows directly into asset prices. Which also tends to enrich those who own said assets, further exacerbating the economic divide between those that have and those that do not. The other problem is, when we live in a fiat, debt based monetary system, you can’t create or QE money without also issuing debt. Money and debt are different sides of the same central bank coin. So, when you hear those clamouring against the massive amounts of growing US government debt, rest assured; central bankers would deem them mere fools. In their eyes, debt doesn’t matter…that is, until it does. Just ask Hyman Minsky.

If you haven’t read any of Minsky’s work, well you should. We are certain that some of you have at least heard of the “Minsky Moment.” A Minsky Moment can be characterised by over-speculation fuelled by cheap money where asset prices that once rose begin to fall precipitously, and leveraged players face exponential losses which they can no longer finance. Here is a great article from the New Yorker dated February 4th 2008; it's as true now as it was back then.

So why did we go through that long diatribe, because we know this moment continues to be thwarted, decades at a time as central banks around the globe pass the baton of QE off to one another. The Federal Reserve has been raising rates, pushing them up from the zero bound, now toward the upper limit of 2.50% (in terms of the Fed Funds rate). They have also been reducing their balance sheet in coordination with these rate hikes. We know full well these rate hikes aren’t because the economies around the globe are booming; it's because they need to give themselves room to manoeuvre come the next 'Minsky Moment'. We understand that a 2.5% Fed Funds rate isn’t much, but if you consider the starting point, we are once again talking about factors, and if we now look at the US government’s total debt, the sheer mathematics should scare you. With the US debt sitting at just under $22trillion dollars, this puts the interest payments per year around $562 billion. In a $19 trillion-dollar economy you can see how quickly this adds up as time moves to the right. Trump cannot even get $5 billion for the wall; now you know what a farce all that spectacle truly is. Its no wonder gold has found a bottom in 2018 (but that's a topic for later in the letter).

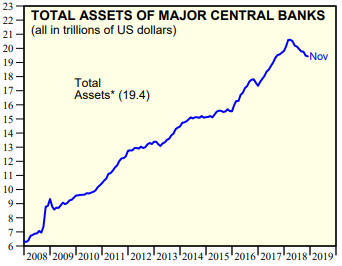

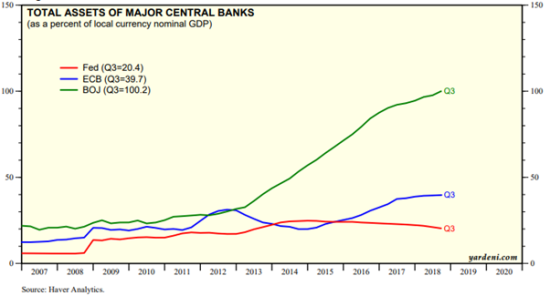

Anyway, with central banks cutting back their asset purchases and with the Federal Reserve continuing to raise rates, it should be of zero surprise to any investors that the global equity markets have been under attack. Yardeni Research posted a couple of great charts in their December issue and we have one right here:

As you can see, 2018 saw more than a trillion dollars being deducted from global central bank balance sheets; just think of this as the first pillar of support to fall from under global equity markets. The mantra of “Buy the Dip” has been so pervasive in the last few years, we figure many are still caught long and wrong here, despite this kind of data staring them in the face. Secondly, despite the jawboning by Trump, Fed head Powell has continued on the rate hiking campaign and it's one we completely agree with. Sometimes a little frugality amongst the over indulgence is a necessary interlude. We understand the conditioned masses are so addicted to cheap money, yet in reality the day of reckoning always comes and it's never a matter of if, but when.

So, to enlighten you with our first call for 2019, the Federal Reserve will raise the Fed Funds rate up one more time to 2.75%, inverting the Fed Funds/US 10yr and the US 2s10 yield curve. The 2s10 has been hovering around the 20bp level for the last 5 months but we figure the Fed will raise rates at their March 19/20th meeting finally inverting this curve shown here:

This provides us with the ground work for our second call for 2019, which is that Q1 for the equity markets may see some carving out of this new-found equity market range. Our view is still outright bearish, yet we aren’t naïve enough to just think an outright sell will not go untested. We also figure a whole host of equity support will be coming in January as long-term liability matchers rebalance their portfolios to reflect this new-found equity market discount. When was the last time you could pick up the FAANGs at such depressed levels? Remember, many managers are still conditioned by the central bank “put” and “QE” lessons not learned are lessons not followed, so we expect this down turn to be a process, not all at once. Anyway, this SP500 chart shows the lows printing into bear territory but the last week of 2018 may see some salvation:

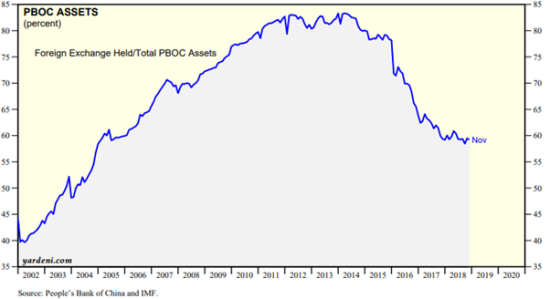

We suspect that the high is in for quite some time, but we will not rule out a run and test from here up toward 2650. Given the fact that the Fed is not expected to hike at the Jan. meeting and that rebalancing may provide some decent support, this call seems logical at the moment. Obviously, things can and do change which brings us to our 3rd call for 2019, and that is China caves on US tariffs and agrees to some concessions. This would obviously be equity bullish and we see it happening sooner rather than later as Trump is a master negotiator and is playing from the power position. Despite the naysayers, we feel the US has the upper hand here. China can ill afford a prolonged tariff spat and it's most noted in their foreign reserve usage which continues to dwindle and is less potent at stemming capital flight out of the mainland. Yardeni posted this next chart and we think it paints a very clear picture of the corner China is being forced into and the validity by which China can ill-afford a prolonged came of chicken with the US:

This tariff disagreement between the US and China is indeed very dangerous and disruptive to the global balance and it is one we are watching very closely. We have talked at length this year as to how trade wars can often turn hostile and end up being hot wars. Given the nature of these superpowers and the continued global jawboning going on, as an outlier call for 2019, this may be the one thing that ultimately breaks the global equity back and if tensions flare and paths are crossed, well then, all bets are off!

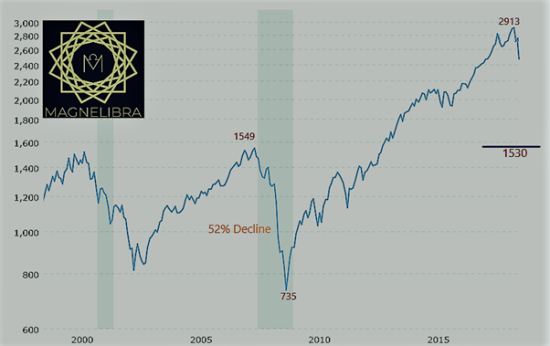

If the SP500 does start to falter, we have to look back as to how far things could potentially run. Just to overlay a potential move that we saw in 2008 and to paint a similar 52% decline we present this chart depicting an SP500 down at the 1530 level, some 38% lower than current levels:

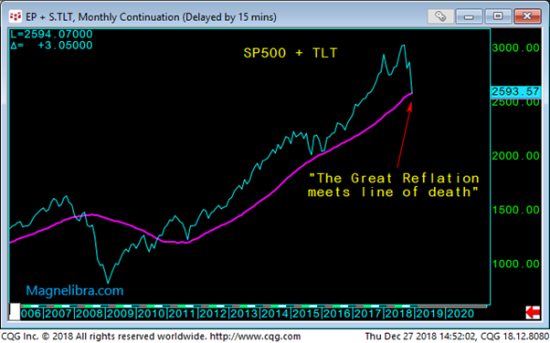

For those that continue to deny such possibilities, we present this next chart, which is the aggregation of the SP500 plus the TLT bond fund. We like to refer to it as the reflation trade, as both equities and bonds seem to benefit. You can obviously see how far we have run since 2009 and now that we have touched the 200-day moving average and bounced, we will simply call that our “line of death.”

Now before you start questioning this doom and gloom, rest assured, we have you covered, as the Central Banks around the globe will no doubt come to the rescue again with a whole host of rate cuts and QE programs. The Fed has given them the room and we suspect if things transpire in 2019 as we think they will - first with some equity stability, followed by a complete drubbing that is tell-taled by a US yield curve inversion come March - the central banks will use their reflating QE printing presses. Just how much can the FED do? Well if we look at just the BOJ and ECB in percentage of GDP terms, we feel the FED has trillions to work with. In fact, just to match the ECB - their ratio of balance sheet to GDP stands at nearly 40% - we would be looking at Federal Reserve to hit total assets of around $7.6 trillion, or a 90% increase from current levels. So, don’t fret and make sure you have some cash in hand and expect opportunities to clearly present themselves! Here is another chart from Yardeni.

We spoke of some of the FAANGs earlier, so let’s take a look at some recent price action in Apple. We talked at length this year about Apple and the fact that they have hit peak pricing and that they're starting to see margin pressure build. We have also noted that they have virtually staked their whole fate on just one product…never a good business decision. We know they have billions of dollars, but we also know they spend around $14.2 billion a year on R&D (2018 SEC 10-k). As far as support, a decent low has been hit here at $148 but ultimately the $134 area seems logical.

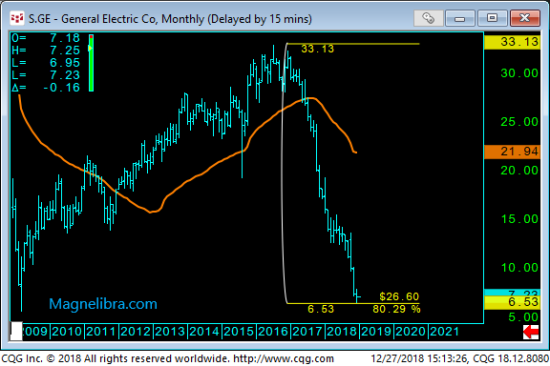

Since we have been referencing the last decades overall move, it seems prudent that we mention General Electric. Remember, in 2007 and 2008, GE, once a beacon of US industrial might, became enamoured with the mortgage, finance and lending business. It cost them billions and eventually good ole’ Warren Buffett had to use Berkshire cash to bail them out, most likely with an implicit guarantee from the US government, which came a few months later, as the FDIC insured nearly $140 billion in GE debt. (NY Times)

Although many will consider this crony capitalism, Wall Streeters just understand it as 'heads I win tails you lose', meaning the closer you are to the governments' largesse, the more likely you are to be bailed out...but we would just rather not be so naïve and understand the system for what it is; imperfect, but a necessary evil. Anyway, look at GE now; it's the same price as a decade ago; maybe they have finally succumbed to decades of malfeasance and mismanagement. GE is down 80% from its highs to its recent lows and is trading exactly where it was in early 2009:

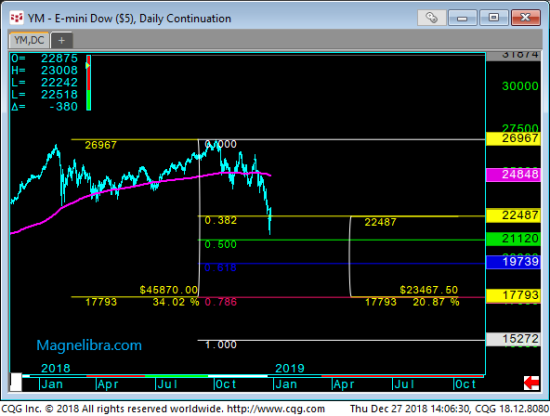

Our next chart is the Dow. As we mentioned previously, equities have thus far reached some decent supports and now the Dow futures sit right on their 38.2% Fib retrace at 22,487. We feel a run up from here to test the 24,800 level should bring in new shorts. Ultimately, we think 2019 will see a drop toward the 17,800 area where a significant rebound will most likely occur on the heels of further central bank expansion.

Moving overseas, we are looking at the DAX future, whereby you can see the absolute drubbing it has taken this year, down some 19.8%. It has, just like the other equity markets reached some decent supports:

So just to recap the equity picture, we feel that Q1 2019 will see a whole host of bottom pickers come into support the markets. First and foremost, the long-term liability players like pension funds and insurers will be rebalancing and adding to their current equity holdings as the recent drubbing will induce such activity. On the flip-side of that you have CTA trend-following sellers looking to enter into what many now believe is an equity bear market. So, all in all, we think the equities move sideways to higher before that fateful March rate hike which will seal their fate. We must be fully cognizant in the midst of this bearish mindset that any positive tariff news will certainly be bullish for equities, so be on the lookout for that as well.

Bonds

As far as the US government bonds, we touched upon the inversion that we expect in the US 2s10 come March and now we will comment on the US government 10-year bond. The recent break of 3% has seen a huge 30bp run toward the 2.70% area. We expect some back and fill here as equities stabilise short term, but we feel the upside to yields is capped based upon a bearish outlook in equities and the fact that the FED is near the end of their hikes. The astute bond players will put the FED in their place and begin front running future rate cuts; this, we feel, will most certainly be on the minds of bond traders in 2019. Our target range for 2019 for US 10-year yields are 3.05% to 2.30% with the upper bound most likely seen into the February refunding (which will most undoubtedly be massive) and the March Fed meeting. The lower bound should be seen later on in the year as the FED pauses and even contemplates reversing course depending solely on the severity of the equity markets moves. As our title suggests, 2019 will be characterised by the Feds inability to remove QE and, once again, its tendency to run to the only solution it knows; more QE, or what Magnelibra has coined as '#QE4EVR'. The following chart depicts the US 10-year in yield and shows the large drop of over 53 basis points from the 3.26% high to the current levels of 2.73%. We expect a return to 2.01% in the long run:

Energy

We haven’t really touched upon the energy markets, and as we do follow them, and considering the absolute about face the Crude market has done this year, we have to opine just a little bit here. We have heard all sorts of production excuses; OPEC arguments as to why Crude basically fell out of bed. Yet we aren’t sure what the true reason is. Could it be that the energy markets are also discounting a global slowdown? This certainly makes sense and so too does the fact that the United States is now the leading producer of oil. In fact, the United States produces nearly 30% more than Saudi Arabia. The Energy Information Administration states that the US produces 15.6 million barrels a day compared to 12.1 million for SA (EIA.gov). Considering this fact and considering this trend is going to continue, perhaps that is more of a reason why Crude, which we will show in this next chart showing the February futures contract, has declined from a high of $76.52 down to its recent low of $42.32, a loss of nearly 45%. Just to put this into perspective, Crude oil was up 35% for the year and is now down 22%. What an absolute whip saw! If we stick with our global slow down then, we should see Crude trade around the $50 level for 2019 (most likely capped by that 2018 high of $76); under $40 and we start to see some other dynamics at play, most notably leveraged producers and their debt piles being once again called into question. So not that we expect a prolonged protraction, but when leverage gets tossed into the mix, fire sales can drive prices certainly below fundamentals:

Metals

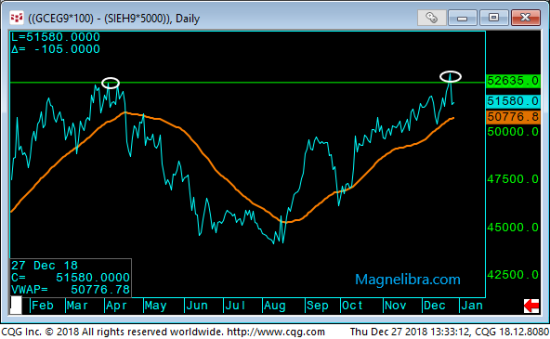

We feel that 2019 will be a great year for the metal market. Gold continues to shine and looks to be in a clear uptrend since the August lows. All this amongst a hiking FED which has also seen the US dollar maintain its strength. 2018 has basically been one big down move in the complex, but the last few months it seems the complex has carved out a nice base and continues to rise. In our most recent note, we highlighted the fact that Gold has been moving higher relative to Silver and recently hit the high of the year in this spread. Noting the double top and prior resistance, Silver has regained some footing vs Gold as depicted in this chart:

We feel both Gold and Silver will reverse their 2018 fortunes and trade above $1,400 and $17 respectively. Here is the February Gold futures chart:

Crypto

In what seems to be a bizarre and overwhelming contrast in respect to Cryptocurrencies this year from last, we can’t help but comment on the digital asset sector. As 2017 came to a close, it was all euphoria in the space and then the floor just absolutely fell out from under it. The speculators that drove the pricing to exponential heights were taken out feet first with damage so swift and severe, many would never recover. Yet we are still bullish on blockchain and its decentralised nature. Innovation in the space will continue and the future will most definitely incorporate blockchain in one way or another.

As far as treating these assets like financial assets, we can’t help but admit our disdain for such folly. Cryptocurrencies should never be financial assets to be swapped for fiat; that is simply a Wall Street incarnation. Rather, they are designed as a function of a particular decentralised payment or information system. The titan of these technologies continues to be Bitcoin. Even after all the damage in 2018, it currently trades at $3,600. Many will say 'it is finished, its worthless, it is down 82% off its highs'. If you take that perspective then yes, we can see the doom one sees. Instead, how about we take a different perspective and say 'its been around for a decade now, it trades at 3,600x the US dollar and its up 21% from September of 2017'. What people fail to realise is that Bitcoin is not an asset in a financial sense, to be swapped for fiat; it is a technology whereby the required cost of usage is Bitcoin itself.

Now we know the SEC has failed to pass any true merit tests in regards to Bitcoin ETFs, but they do so undoubtedly at the request of the Federal Reserve itself. You see, dear reader, Bitcoin is a competitor to fiat money, plain and simple. And it is in that fact alone that all necessary measures will be taken to ensure that it never becomes mainstream. Whether or not the powers that be succeed is still in question, but for now, we suspect that blockchain will continue to advance and that Bitcoin will continue to be the preeminent asset amongst its digital peers. So that is the Magnelibra take on it; we are bullish on the technology, and our only real opinion is that you treat it as a technology and understand that the future, albeit uncertain, will most certainly have a use for it somewhere. Treat it as a technology never to be converted to fiat, end of story.

That covers most of what we expect from our financial market perspectives. The other things we are keeping an eye out for in 2019 are more scientific in nature. Some of the key words you should be aware of are, grand solar minimum, cosmic rays and plasma physics. Be on the lookout for increased volcanic activity; all of this is related in some way, so we want you to be aware of it. You have been told that the Earth is warming, but like markets, the Earth has cycles as well, periods of warming and periods of cooling. Our job is to peak your interest in things we believe matter, and these things matter!

As we bring 2018 to a close, we can’t help but thank all of our readers, clients and those that have helped us bring Magnelibra to fruition. It has been a long time in the making and we can’t thank everyone enough. We continue to strive and bring you the kind of research that we don’t think you will find anywhere else. We look to drive your trading and investing instincts so that you can make better informed decisions. We hope this year’s 2019 outlook has given you enough of a glimpse through the lens by which we view chaotic and volatile markets. The Magnelibra Blue Dragon Discretionary program will look to take advantage of all the opportunities we just outlined in this outlook. We gave you a brief overview by which we will look to construct our trades in the coming year. As always, we don’t expect to be right on all accounts, but rather we look to be tactical in our approach, adaptable in our execution and mindful always of the sheer fact that markets can and often do, move with conviction, without hesitation and most certainly, without distinct notice. It is within the Blue Dragon Program that we construct a long/short model so that we can avoid the large pitfalls extreme volatility creates. Our goal is to maintain a liquid strategy designed to generate uncorrelated risk adjusted returns. We hope you have a very safe and joyful New Year, cheers!

**********

Mike Agne is Portfolio Manager at Magnelibra Capital Advisors

DISCLAIMER: For Educational purposes only. This is not a solicitation to buy or sell commodity futures or options on neither commodity futures nor an endorsement for the purchase and sale of an ICO, Cryptocurrency or any digital asset and should not be construed as such. The risk of trading securities, futures and options can be substantial and is not for everyone. Such investments may not be appropriate for the recipient. The valuation of futures and options may fluctuate, and, as a result, clients may lose more than their original investment. Nothing contained in this message may be construed as an express or an implied promise, guarantee or implication by, of, or from the author Mike Agne owner of Magnelibra Capital Advisors LLC (MCA) and the website blog, which can be found at www.econemotions.com. All rights are reserved. We will never claim that you will profit or that losses can or will be limited in any manner whatsoever. Past performance is not necessarily indicative of future results. Although care has been taken to assure the accuracy, completeness and reliability of the information contained herein, (MCA) makes no warranty, express or implied, or assumes any legal liability or responsibility for the accuracy, completeness, reliability or usefulness of any information, product, service or process disclosed.

***

The views expressed in this article are those of the author and do not necessarily reflect the views of AlphaWeek or its publisher, The Sortino Group

© The Sortino Group Ltd

All Rights Reserved. No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or scanning or otherwise, except under the terms of the Copyright, Designs and Patents Act 1988 or under the terms of a licence issued by the Copyright Licensing Agency or other Reprographic Rights Organisation, without the written permission of the publisher. For more information about reprints from AlphaWeek, click here.