Unigestion Presents Its Macro And Investment Themes Outlook For 2018

Following a better than expected 2017 for most asset classes, we expect the New Year to present some challenges:

- The ‘Goldilocks’ economic effect is unlikely to persist into 2018

- Global economic growth should remain well supported, but inflation is expected to push higher driven by wage growth among other factors

- Monetary and financial conditions are likely to tighten in 2018 as central banks worldwide start to unwind their ‘easy’ monetary policy stance

From an asset allocation perspective, our tactical positioning will follow three key themes:

- Central bank tightening should be less worrying if exposure to duration-sensitive assets is reduced

- Maintaining or increasing exposure to equities and commodities could benefit from an acceleration in inflation

- Relative value strategies have the ability to generate non-directional returns.

1. The ‘Goldilocks’ economic effect benefitted investors in 2017

In our macro and investment themes outlook for 2017, we expected to see higher growth and inflation, which would result in strong returns for growth-oriented and real assets. In hindsight, we were proven to be both right and wrong. Growth figures were consistently upgraded throughout the year, but inflation undershot expectations in most areas, despite cyclical improvements and tight labour markets.

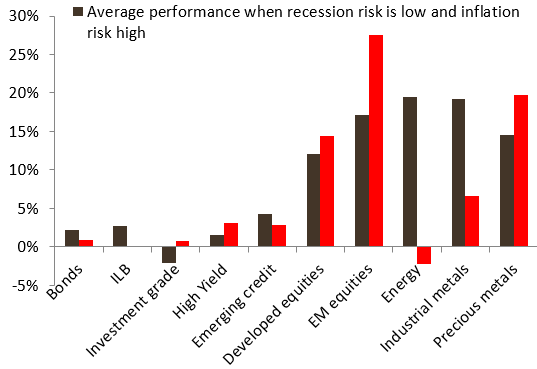

Even so, the stars were aligned for most assets in 2017. A ‘Goldilocks economy’ of low inflation, synchronised growth, healthy corporate earnings and a continuation of loose monetary policy from central banks allowed risk assets to outperform significantly. Figure 1 perfectly illustrates the scale of 2017’s returns – thanks to the ‘Goldilocks’ effect – and shows that most asset classes also overshot the average expected return for a similar macroeconomic environment[1].

2. But the economic backdrop will likely be less supportive in 2018…

Unfortunately, some of the supportive factors behind 2017’s robust returns are unlikely to persist in the New Year:

Overall, we expect world growth to remain solid and synchronised, allowing World GDP to grow above potential for a second consecutive year. According to International Monetary Fund (IMF) forecasts, the output gap for advanced economies will rise from -0.1% in 2017 to 0.3% in 2018[2].

Yet, we believe the era of low inflation will end sooner rather than later. This view is based on several factors that we expect to push inflation higher next year.

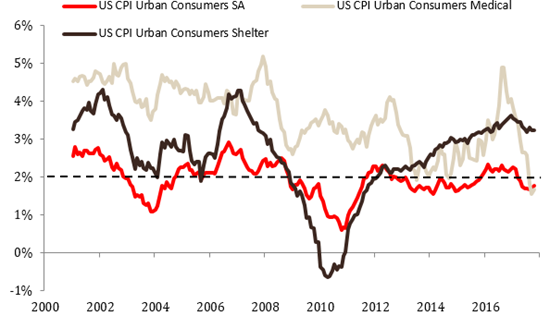

- Firstly, this year’s undershoot in US inflation, which has been defined by the Federal Reserve (Fed) president as being “a mystery”, has in fact been attributed to a-cyclical components, such as falling medical costs[3], which we believe will be less important going forward (see figure 2).

- Secondly, we recognise the theory of the Philipps Curve that links unemployment rates to wage growth. This link is likely to become increasingly important in generating inflation pressure next year, given we expect unemployment rates to remain low among developed and emerging countries which should lead to a rise in salaries - a scenario that is already taking place in Japan, the US and Germany.

- Thirdly, the rise of producer price inflation in recent months should push consumer inflation higher as a secondary effect

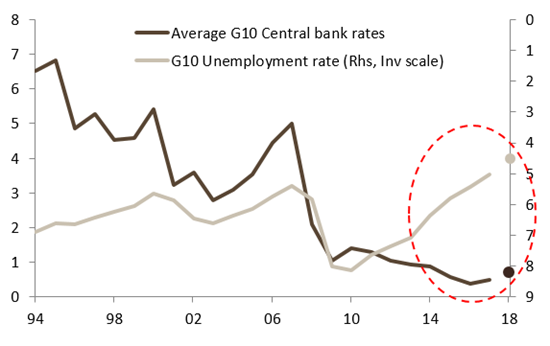

Monetary and financial conditions to tighten. As already stated, the cyclical improvement has been massive, globally, over the last 2 years. However, few central banks have considered this positive trend to be solid enough to modify their accommodative monetary policy stance. Figure 3 illustrates how the gap between cyclical improvement and monetary policy stance has widened since quantitative easing (QE) became more generalised in the aftermath of the financial crisis.

Our main conviction for 2018 is that the era of ‘easy money’ will come to an end. There is already some evidence of this shift. For the first time since the financial crisis the ratio between “easing” and “tightening” activity moved in favour of the latter in 2017, thanks to interest rate hikes from the Fed, the Bank of England and the Bank of Canada. Moreover, the European Central Bank (ECB) announced a reduction in its bond purchasing programme, which is expected to be the first step before hiking.

We expect the move away from ‘easy money’ to amplify next year. In our view, employment and inflation gaps have been reduced enough to justify this shift in monetary policy, while any arguments favouring the maintenance of ‘easy money’ become less and less relevant. Moreover, an increasing number of central bankers have highlighted the negative effects on financial stability and capital allocation of monetary policy being too loose. This leads us to believe that central banks will adopt a more hawkish stance in 2018.

3. If the music stops – or changes – we can still adapt the rhythm of our dance

In 2007 the Citigroup chief executive, Chuck Prince, said “when the music stops, in terms of liquidity, things will be complicated. But as long as music is playing, you’ve got to get up and dance.”

We are under no illusion that 2018 is unlikely to witness the robust returns that have been enjoyed this year; in fact, we expect the ‘song’ to change markedly. We have previously related the macro environment of the last two years – low volatility, with global growth at close to potential at a time of no inflation surprises – to the Daft Punk song: Harder, Better, Faster, Stronger (albeit with some artistic license): the closer global growth stays to its long-term non-inflationary potential, the lower the risk of an economic shock, the longer central banks can stay behind the curve and the higher growth assets can go.

In 2018, we expect inflation to shift from undershooting to overshooting expectations; risk is likely to remain behind the curve, which could become unsupportable for central banks; and, therefore, this could be the year of monetary policy surprises. In this light, Daft Punk’s song again applies, although the overall dance is likely to be less celebratory this year: the stronger global growth, the higher inflation risk, the faster central banks adjust policy and the harder “quantitative easing (QE) reversal” could be.

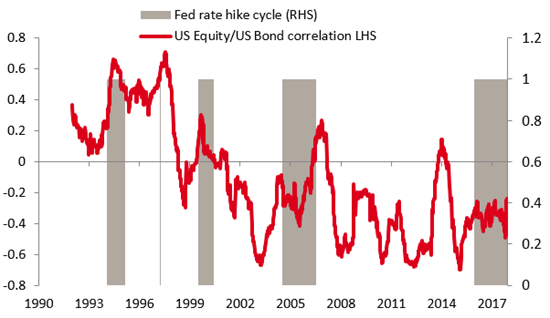

With this in mind, correlation and volatility could change dramatically going forward, as illustrated by figure 4 which shows the correlation between US bonds and US equities during previous rate hiking cycles by the Fed.

In effect, central bankers will be “DJ market maker” next year and our tactical positioning will, therefore, be based on three key themes:

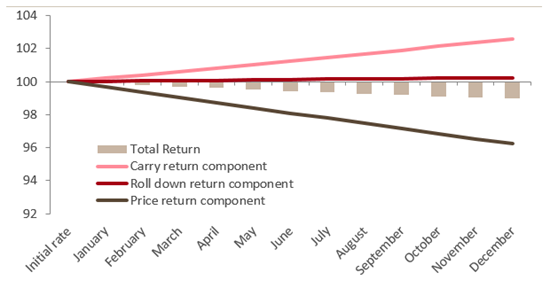

In our view, potential central bank tightening is less of a worry if portfolio exposure to duration-sensitive assets is reduced. We expect the combination of higher inflation, synchronised global growth and central bank action to drive long-term bond yields higher and believe that the Barclays Global Treasury Index could post negative returns in 2018 for the first time since 1994. As shown in figure 5, our calculations indicate that a rise of 50bp in US 10y sovereign bond yields over the next 12 months could be enough to cancel out any positive returns generated by carry and roll-down.

Given our forecasts on the macro side, we do not believe it’s unrealistic to expect that US 10y bond yields could near 3% by the end of next year, while German bond yields could reach 0.9%. This increase in bond yields would likely be driven by rising inflation and growth premiums. Nevertheless, we are not expecting the bond market to crash nor for another taper tantrum to take place. In our view, central bankers learned from this previous episode and have endeavored to significantly improve their communication strategies. Moreover, these anticipated increases in yields are far from those observed in 2013, when US 10y yields jumped 130bps and German 10y yields spiked 95bps (Source: Bloomberg).

There are ways to benefit from an acceleration in inflation – for example a preference for equities and commodities. The role of easy money has been crucial in supporting asset prices over the last five years. However, we believe tighter financial conditions could limit the upside potential for growth-oriented assets going forward.

Within cyclical assets, we expect equities to continue benefitting from the stable growth environment, US fiscal stimulus and rising consumption and this backdrop should be supported by higher disposable income and the positive wealth effect going forward. Moreover, equities should continue to provide the highest carry among traditional assets, such as sovereign bonds, credit spreads and commodities. For example, the dividend yield of the S&P 500 is 150bps above the real yield on 10y US Treasuries (Source: Bloomberg).

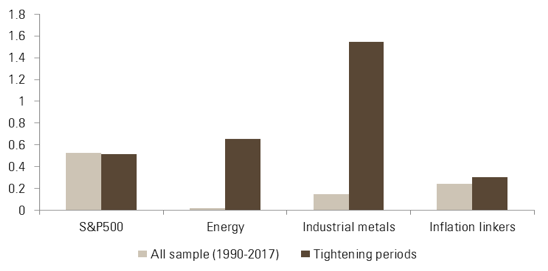

Finally, and most importantly, equities have the potential to deliver positive returns in 2018 despite central bank tightening, as illustrated in figure 6, although we do not expect these returns to reach double digits. Firstly, because valuations are higher than they were 2 years ago, limiting the potential of price/earnings expansion. Secondly, because equity markets could be impacted by tighter profit margins reflecting the rise in wages mentioned earlier. Commodities offer attractive protection in case of reflation as after several years of supply and demand imbalance, commodity markets have evened out their overcapacity issues. The New York Fed[4] and ECB[5] have highlighted that increased demand has supported the price recovery for commodities this year. On the top of that, commodities could provide diversification as correlations with other traditional assets are close to 0.

Relative value strategies have the ability to generate non-directional returns.

We believe it is preferable to lower the portfolio’s beta exposure by implementing relative value trades, i.e. moving from a “beta” style to one more focused on “alpha” generation.

Looking ahead to 2018, our anticipated relative value trades include being long developed equities at the expense of credit spread on the basis of their expected superior liquidity profile; long Japanese and European equities versus equities in the US and UK on the back of more attractive valuations and fewer expected policy risks. In terms of sectors, financials and energy are preferred over defensive sectors, as these are more dependent on duration. In the foreign exchange FX space, we favour the Japanese yen and euros because these both have the potential to offer defensive characteristics in case of a short-term equity downturn and upside potential if monetary policy shifts from QE to exiting QE.

**********

Guilhem Savry is Head of Macro and Dynamic Allocation at Unigestion

Footnotes

- [1] Macro regimes are identified thanks to Unigestion’s Nowcaster indicators that assess macroeconomic context in real time. Our GDP Nowcaster and Inflation Nowcaster track the probability of being in recession and/or inflation surprise regime respectively.

- [2] World Economic Outlook, October 2017, IMF

- [3] Macro FRBSF Economic Letter 2017-35 What’s down with inflation, Tim Mahedy and Adam Shapiro

- [4] Macro New York Federal Reserve paper: ‘Oil price dynamics November 2017’

- [5] European Central Bank paper: ‘Financial Stability Review November 2017 – macro-financial and credit environment’

This document is addressed to professional investors, as described in the MiFID directive and has therefore not been adapted to retail clients. It is a promotional statement of our investment philosophy and services. It constitutes neither investment advice nor an offer or solicitation to subscribe in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment. These are not suitable for all types of investors. The views expressed in this document do not purport to be a complete description of the securities, markets and developments referred to in it. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Data and graphical information herein are for information only. No separate verification has been made as to the accuracy or completeness of these data which may have been derived from third party sources, such as fund managers, administrators, custodians and other third party sources. As a result, no representation or warranty, express or implied, is or will be made by Unigestion as regards the information contained herein and no responsibility or liability is or will be accepted. All information provided here is subject to change without notice. It should only be considered current as of the date of publication without regard to the date on which you may access the information. Past performance is not a guide to future performance. You should remember that the value of investments and the income from them may fall as well as rise and are not guaranteed. Rates of exchange may cause the value of investments to go up or down. An investment with Unigestion, like all investments, contains risks, including total loss for the investor.

***

The views expressed in this article are those of the author and do not necessarily reflect the views of AlphaWeek or its publisher, The Sortino Group

© The Sortino Group Ltd

All Rights Reserved. No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or scanning or otherwise, except under the terms of the Copyright, Designs and Patents Act 1988 or under the terms of a licence issued by the Copyright Licensing Agency or other Reprographic Rights Organisation, without the written permission of the publisher. For more information about reprints from AlphaWeek, click here.