The US Dollar In 2022: Cautiously Bullish

Partner Content provided by The Lykeion

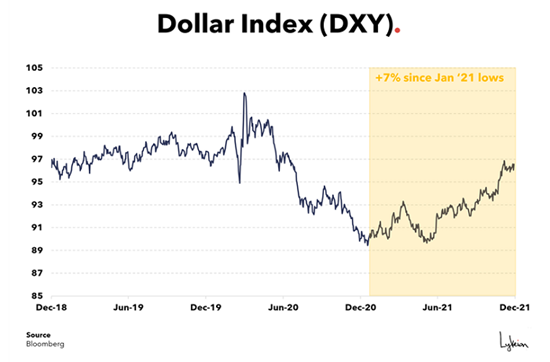

At the end of 2020, there was an overwhelming consensus for the US dollar to decline in 2021. The Dollar Index (DXY) however, gained over 7% since its low in early January.

The bearish consensus view at the end of last year was built upon two major expectations for 2021:

- The US twin deficits (government budget deficit and trade deficit) would undermine the US dollar, and

- The reflation trade (fueled by government stimulus) would support coordinated global economic growth.

Twin Deficit: The bear case of the ‘twin deficit’, where additional debt issuance (from the government) and money printing (from Central Banks) would lead to a continued loss of confidence in the US dollar versus other major currency blocks, has been made for many years, but even more so in 2021 given the size of the pandemic-related fiscal and monetary support.

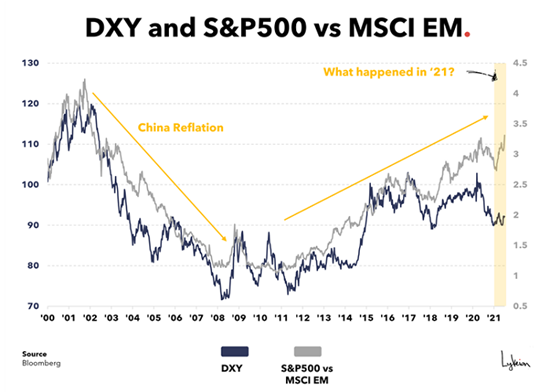

Reflation: At the end of 2020, the reflation trade was a major argument in favor of dollar weakness as, over the previous 20 years, similar economic environments saw (1) emerging market equities outperform, (2) the US dollar underperform, and (3) commodities rise (most notably during the period of China growth from 2002 to 2010).

In November 2020, two events supported the reflation narrative:

- Biden’s US Election victory, which was expected to spark a wave of loose fiscal policy (government spending) and an equally accommodative Fed.

- The announcement and rollout of vaccines, which was expected to re-open the global economy, with the rebound expected to be more prominent in Emerging Markets.

At the end of 2020, the reflation trade appeared to be in full swing. Commodity prices were soaring, the DXY was on its way to a loss of over 10%, and bullish sentiment on EM stocks was a consensus trade for 2021 (according to the Bank of America Fund Manager Survey).

Why did the consensus for dollar weakness in 2021 turn out to be wrong? It was largely due to:

- Global economic growth was not as synchronized as anticipated to create true reflation (countries staggered their reopening as opposed to altogether)

- Inflation

- Consensus in positioning

2021: Staggered Economic Growth

Recurring strains of COVID, supply chain bottlenecks, and divergent policy meant that global growth was insufficiently synchronized in 2021 to create true reflation. Emerging Markets stocks underperformed, whilst the DXY rebounded off the lows. Commodities did rise, but this was the red herring of inflation from bottlenecks, not economic growth.

This uneven pace of global growth was generated by a divergent policy response in both style and sequencing. Let’s look at two of the most important engines of global growth: the US and China.

The US Fiscal Response:

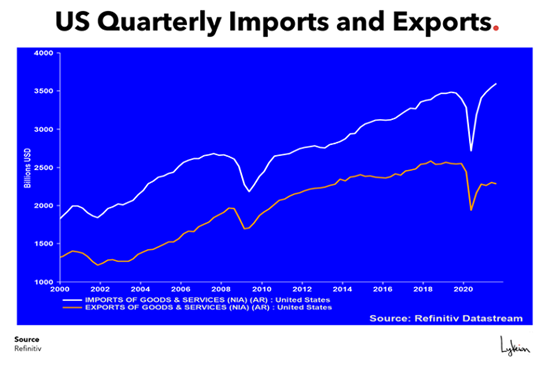

- The US implemented demand-side policies that boosted the consumption of durable goods, helping the economy rebound at a faster pace than many global peers. This can be seen below, with US imports having recovered better than exports.

China Rebalances:

- China was one of the first nations to recover from the pandemic, using supply-side policies in 2020 that focused on maintaining factory production, rather than demand-side policies to support household consumption.

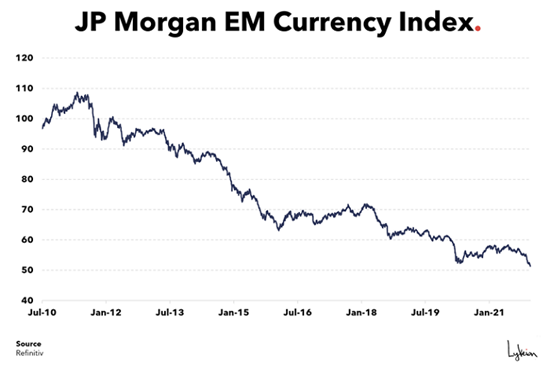

- During 2021, China implemented strategies such as 'Common Prosperity', to help rebalance the economy away from leverage and inequality. This redirection would impact other export nations (such as Emerging Markets) whose growth models had historically benefitted from Chinese demand.

- The consequential impact of this can be seen in emerging market currencies, which have severely lagged the DXY (a basket of global currencies vs the US dollar and heavily weighted by the Euro). By the end of 2021, the JP Morgan EM Currency Index had made a new ten-year low.

2021: Inflation (not Reflation)

The combination of loose fiscal policy and higher inflation was expected to undermine global real yields, especially in the US (which would have led to a lower US dollar). But:

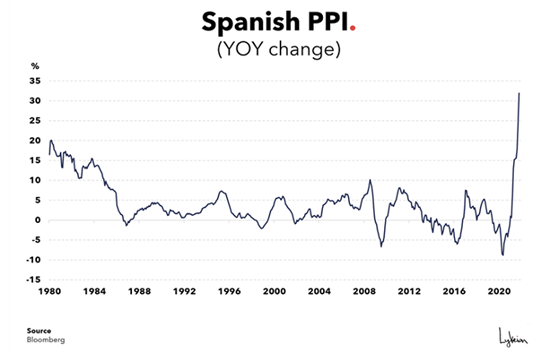

- Although US inflation has soared, it has been exceeded in many other regions. Spanish Producer Price Inflation (PPI) is at its highest level, 31.9%. No Bueno.

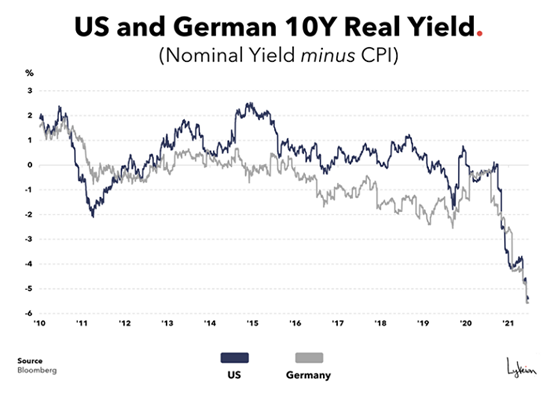

- US real yields have collapsed, but that decline has been matched in other regions. Real yields on the German Government 10-year bond are at the same level as the US 10-year treasury. The decline in real yields has therefore not undermined the US Dollar on a relative basis.

Adding to this, the boost from fiscal policy, the switch out of services and into finished goods, and the inability of supply chains to cope led global commodity prices higher. Higher raw material prices meant different things for the US and elsewhere:

- For the US, this was both inflation and reflation (i.e. higher prices and economic growth).

- For the rest of the world, this was inflation, not reflation - it lacked the accentuated economic growth profile of the US given that, without China's demand, there was very little real growth in other regions.

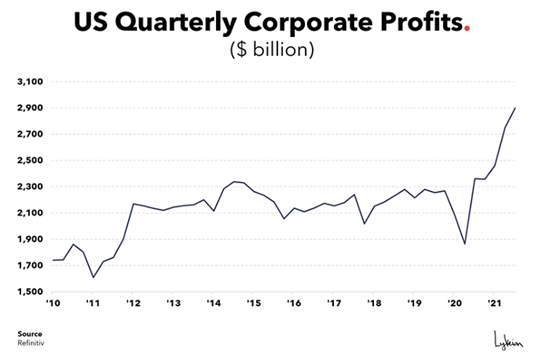

Within the US, companies were able to pass on higher prices and generate higher margins (consumers had extra cash that could absorb those higher prices, whilst companies focused on cost reductions), leading US corporate profits to surge during the pandemic after five years of going nowhere.

Ironically, this allowed US stocks to remain attractive despite (or because of) the fiscal policy that many had expected to undermine the US dollar, which led to a persistent bid for US equities and, consequently, US dollars.

All in all, inflation in the US led to higher economic growth, and it had less of an impact on real yields, both of which helped the USD perform well in 2021.

2021: The Consensus in Positioning

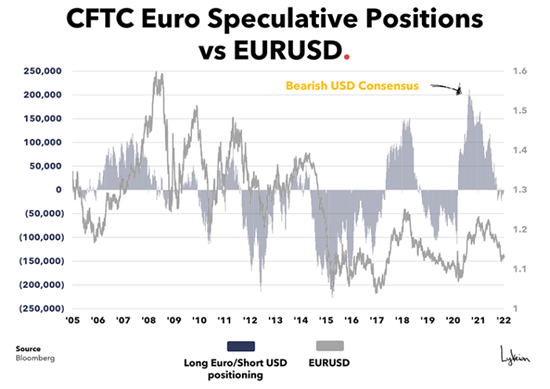

At the beginning of 2021, the non-commercial (or speculative) longs in the Euro versus the US dollar were close to an all-time high (i.e. investors were very bearish on the US dollar). After the combination of Biden’s victory and the positive vaccine news, investors were anticipating the global reflation trade in 2021, buoyed by a strong performance from many commodities.

The consensus of strategists was matched by a consensus in positioning (strategists and the market don’t always agree – on this occasion they did).

Historically, however, once the positioning (bear US dollar) begins to turn from an extreme, it tends to keep going for a while, with the Euro usually falling by 10% or more (which is what we saw at the beginning of 2021).

Investors are far more constructive toward the dollar in 2022 but positioning is far more neutral than at the beginning of 2021.

Can the dollar have a second consecutive year of gains? The key determinants for 2022 are similar to 2021:

- Divergent Fiscal and Monetary Policy

- Supply Chains Constraints

- Positioning and Technicals

2022: Divergent Policy

Going into 2021, Fiscal and Monetary Policies among different countries was fairly harmonized, but the turn into 2022 presents a different landscape.

High vs Low Yielders:

- Fed Chairman Powell, at the December FOMC, outlined a path of policy tightening via a faster pace of tapering bonds purchases and higher interest rates (the release of the minutes this week sparked a significant market sell-off). The US joins a group of countries who are, for now at least, in the tightening camp, where bonds also have attractive levels (in relative terms, let’s be clear) of yields for investors.

- Other regions, such as the Eurozone, Switzerland, and Japan are expected to keep their policy on hold. In many cases, their policy rates and bond yields are already in negative territory, creating significant opportunities for additional divergence.

- There are signs, however, that tighter policy in the US may cap longer-dated bond yields by reducing the expectations for further inflation (tighter policy means increased yields on the short end and lower long term inflation expectations, capping the long end of the curve creating a “yield curve flattening" environment… try to use this sentence as an ice breaker next time you’re in a bar and see what happens). If that materializes, tighter policy may not be as supportive of the US dollar after all.

On balance, divergent policy should favor dollar strength, but it could also push longer-dated yields down to unattractive relative levels, capping the upside.

China:

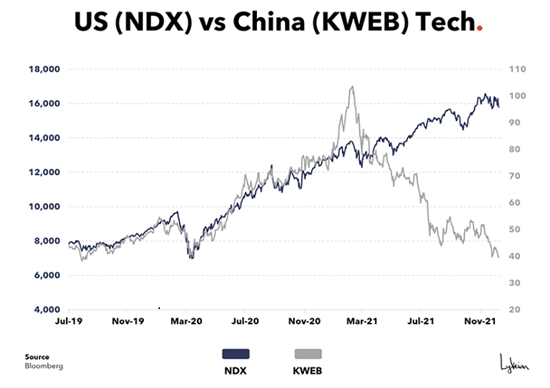

- China is expected to maintain its policy of ‘Common Prosperity’ in 2022. China’s regulatory oversight in 2021 has impacted the performance of the tech sector, which in turn has an impact on broad-based emerging market indexes.

- China’s property sector, which is a large component of the Chinese economy (directly accounting for around 15% of GDP) is also under pressure with the issues around Evergrande having spread to other property developers (though it should be firmly understood by now that Evergrande was NOT a Lehman moment… looking at you FinTwit extremists). Policymakers will not want to lose control of the rebalancing process, especially if the US is embarking on a tightening cycle (though our survey says they’re not… and our survey participants have never been wrong. Ever.).

- An easing of macroprudential policy in China could initiate a relief rally that helps broad-based EM equities perform better. This would be supportive of EM currencies versus the US Dollar. That’s not our base case though.

Current policy in China is negative for other EM currencies as the rebalancing tightens liquidity, and thus Chinese demand. It would require a change in policy stance to fundamentally change this.

2022: Supply Chains Constraints

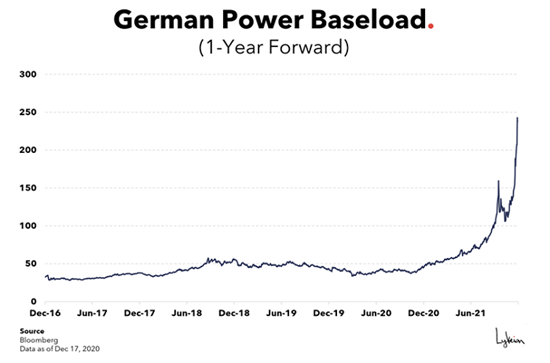

- Supply chains remain impaired, leading Energy prices to soar across Europe.

- Higher commodity prices that reflect higher demand can be a positive for margins, but higher prices without a rise in demand will tend to erode margins. The US is not suffering from the same energy issues as Europe, nor is it seeing the same margin compression.

- Supply chains should normalize (though no one seems to have a reliable answer to ‘when?’), and energy prices should recede, but Europe is currently a prisoner of geography given its reliance on energy imports.

- Until these issues are resolved, European companies will either have to swallow these input costs (at the expense of margins) or pass the costs on (at the expense of demand).

- That being said, energy demand in Europe during the winter is about as inelastic as insulin is for diabetics. So, we’d expect to see demand stay strong (i.e. so people don’t freeze), while European governments continue to subsidize energy costs. At least until the Spring.

Energy issues will, therefore, remain a drag on the outlook for the Euro, but they could be resolved in a short period of time. US corporates appear to have better pricing power for now.

2022: Positioning and Technicals

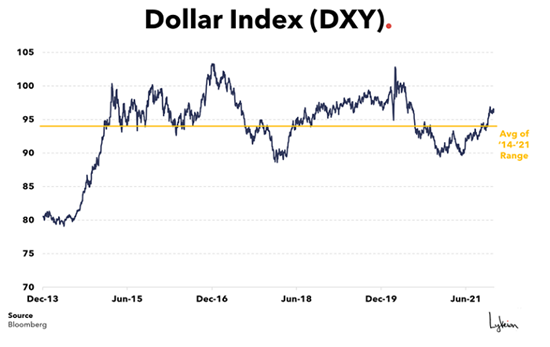

- Despite the strength in the US dollar over the last year, the DXY has merely returned to the middle of the six-year range.

- The dollar, in its broadest sense, is overbought today. Consensus has shifted from extreme bearishness to mild bullishness. This is reflected in positioning, which is less extreme, having recently reached a neutral speculative position.

- The DXY has also seen some major inflection points (higher and lower) through previous year-ends. Although this is a tiny sample size, it’s still worthy of a note.

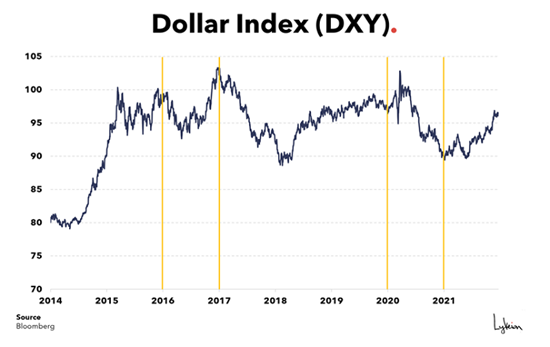

The current rate of change in the dollar has also been relatively gradual when compared to 2014. A rapid move can accelerate the relationships between the dollar, emerging markets, and currencies.

Wrapping it all up

This all means that, for 2022, we would expect:

- The dollar to rise against low-yielding currencies (Euro, Yen, and Swiss Franc).

- In the absence of a policy U-turn in China, the dollar should do well against broad-based EM currencies.

- The dollar may struggle against commodity currencies (like the AUD), especially if those commodities are energy-related.

The expectation for a stronger USD in 2022 is in stark contrast to the bearish consensus for 2021. But the view today is not as extreme as it was at the end of 2020 given that positioning is now much more neutral. Cautiously bullish, that sums it up well.

**********

Roger Hirst is Editor, Macro, at The Lykeion

***

The views expressed in this article are those of the author and do not necessarily reflect the views of AlphaWeek or its publisher, The Sortino Group

© The Sortino Group Ltd

All Rights Reserved. No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or scanning or otherwise, except under the terms of the Copyright, Designs and Patents Act 1988 or under the terms of a licence issued by the Copyright Licensing Agency or other Reprographic Rights Organisation, without the written permission of the publisher. For more information about reprints from AlphaWeek, click here.