Volatility in Transition

In this piece, we will examine prior transition periods from low-volatility to high-volatility regimes and compare such periods to our current markets. We will then answer the question: Are we transitioning from a prolonged low-volatility to a prolonged high-volatility regime?

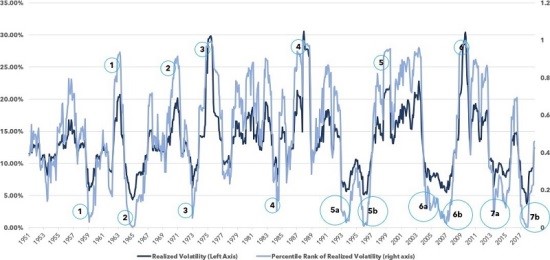

Since 1950, Realised Volatility (as defined as the rolling 12-month standard deviation of returns of the S&P 500) has bottomed seven times: 1959, 1964, 1972, 1984, 1995, 2007, and most recently in 2017.

On average, 41 months following these bottoming periods, Realised Volatility subsequently spiked into its 90th percentile in 1962, 1970, 1974, 1987, 1998, 2008, and most recently to-be- determined.

Rolling Annualised Realised Volatility: 1950-2018

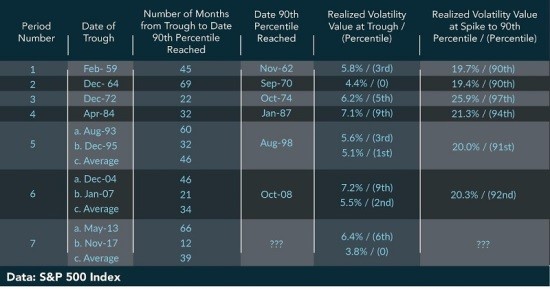

The table below shows the dates and values associated with the above commentary:

History of Troughs to Spikes in Realised Volatility Since 1950 to Present (as circled in the chart above)

The above analysis shows that, on average (including the two “W” volatility bottoms of 1993-95 and 2004-07), the time between these troughs and spikes was 41 months. The average increase in Realised Volatility was from 5.9% to 21.1%.

Of note are potentially three key similarities between Periods 5 and 6 with current volatility regime (Period 7):

- In Periods 5-7, volatility made a “W”-shaped bottom

- In Periods 5-7 the trough occurred during the middle of a Fed hiking cycle

- In Periods 5-6, the spike higher in volatility occurred at or near the end of that hiking cycle

Given the recent comments by our Fed Governors, such characteristics resonate with our current Period 7.

Although the time of elevated Realised Volatility in Period 5 included all-time market highs, the time of elevated Realised Volatility during Period 6 coincided with the financial crisis. Therefore, market direction does not always correlate to the direction of volatility. Both “bull” and “bear” markets can experience similar levels of Realised Volatility. To be sure, from August 1998 (the first month to reach the 90th percentile in Period 5) to August 2000 (the high in the S&P 500), the S&P 500 rallied approximately 60%. Yet, over that same period, 11 of the 24 months included Realised Volatility in the 80th percentile or greater.

We are in the 39th month of our current low-volatility trough and have begun to accelerate higher during 2018. In March 2018, Realised Volatility reached into the 8-9% range. By November, that figure had accelerated into the 12-13% range of Realised Volatility.

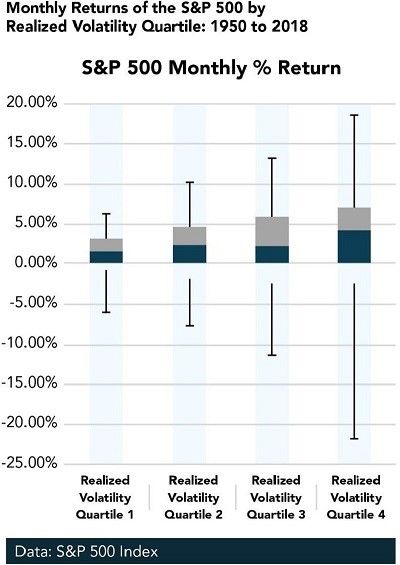

Over the last five years, market participants have experienced a prolonged low-volatility regime in which they may have grown accustomed to relatively low monthly swings in the S&P 500. Characteristic of the bottom quartile of Realised Volatility, the S&P 500 has primarily had monthly returns typically ranging from +/- 3%. As we have transitioned into 2018, Realised Volatility has moved into the second quartile, or an environment in which monthly returns in the S&P 500 typically range from +/- 5%. Should markets follow historical patterns and continue to march toward the top quartile of monthly returns, market participants should be prepared to endure market swings of upwards +/- 10-20%.

VIX Levels and Trends in Transition

Observing the behaviour of the VIX Index since 1990, one can remark on several characteristics (reference the below points with the chart below):

- The VIX Level around 16-17 is a critical historical level for both support and resistance (dark blue horizontal line)

- An upward trend in the VIX ushers in the transition to a higher-volatility regime (green upward trend-lines)

- The upward trend usually carries with it an initial spike (red circles), a retest of the trend-line (red arrows), and then a move higher into a new regime

- Once established above or below the 16-17 range, VIX congregates above or below the historical support/resistance line for an extended period of time (light blue shaded areas)

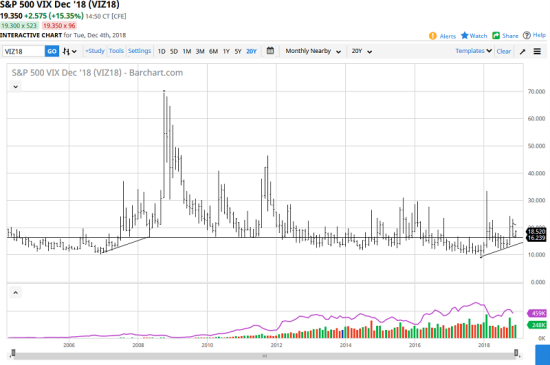

VIX Levels and Trends in Transition: 1990 to Present

In taking a closer look into the similarities between the 2008 and present periods in the VIX Front-Month Futures, we see the same dynamics at play: a respect in the 16-17 support/resistance line, a trend upward initiated by a spike and followed by a retest of the support line.

VIX Front-Month Futures: 2004 to Present

Source: Barchart

Conclusion

None of the above should be construed as a forecast that we are indeed transitioning into a higher volatility regime. If any statement is true about markets it is that they behave in their own way and in their own time. That said, the patterns are clear that moves into the lower percentiles of Realised Volatility have historically produced sharp snap-backs into higher- percentile volatility regimes. We are in the 39th month (averaging time since the May 2013 and Nov 2017 troughs) since the bottom of our latest Realised Volatility period. On average, it has taken Realised Volatility approximately 41 months to then make a move into its 90th percentile. As a warning, the late 1990's has taught us that increased volatility does NOT necessarily mean bear markets! The S&P 500 has made both all-time highs as well as corresponded with catastrophic bear markets in the context of higher volatility regimes.

In addition to the analysis of Realised Volatility regimes, understanding how the VIX Index and VIX Front-Month Futures transition can help put additional context around inflection points. It would seem that both the VIX Index and VIX Front-Month Futures are telegraphing a potential move into a higher-volatility regime—marked by the pattern of the initial spike off the trough, a retest of the historically significant resistance/support levels, and lastly followed by a move higher.

Given the above data and analysis, a higher-than-normal probability exists that we are in the midst of a prelude to a higher volatility regime regardless of the direction of the S&P 500.

**********

Timothy R. Jacobson, CFA and Lawson E. Stringer are Managing Partners at Pearl Capital Advisors

This presentation is for informational purposes only. These results of the Pearl Hedged VIX program (“Program”) are compiled by Pearl Capital Advisors, LLC and are unaudited and may be incomplete or even inaccurate, although are deemed to be generally reliable. None of the results or analysis included herein should be construed as an offer to sell. Investors should consult their own adviser, legal, and tax consultants before making any investment decision. Individual accounts may vary in performance depending on size, funding level, and fee structure.

***

The views expressed in this article are those of the author and do not necessarily reflect the views of AlphaWeek or its publisher, The Sortino Group

© The Sortino Group Ltd

All Rights Reserved. No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or scanning or otherwise, except under the terms of the Copyright, Designs and Patents Act 1988 or under the terms of a licence issued by the Copyright Licensing Agency or other Reprographic Rights Organisation, without the written permission of the publisher. For more information about reprints from AlphaWeek, click here.