Was There A Leading Indicator For The Broad-Based Equity Market Sell-Off?

Given the events of the past couple of weeks, this week for my article I want to steer away from the topics of my typical pieces and speak to the current equity market sell-off and look to see whether there was a leading indicator to what ended up being the fastest equity correction in history. The correction wasn’t limited to equities, of course; with it went bitcoin, oil and many other commodities. The traditional safe havens of gold and sovereign bonds didn’t provide investors a hedge either.

I spoke about this fear and how I would mitigate it in my piece published on January 21st. I said:

“Given the current macroeconomic climate, what is my investment philosophy in terms of portfolio construction?”

To summarise, my fear was three-fold:

- the artificial equity bubble bursting;

- the loss of protection in that scenario; and

- the increased positive relationship between the traditional asset classes.

I said that to make up for the loss of the high negative correlation, especially with my degree of fear of an equity burst in the near future, I believed family offices and institutional investors needed to increase their allocations into more uncorrelated products, than they have traditionally, to lower the hurt that would come from an equity market correction. Given how the traditional asset classes have become increasingly correlated with each other, I said that it is extremely important that investors expand into more non-traditional markets in order to find truly uncorrelated returns via different market/price drivers and return behaviours."

I often speak about the physical economy and the financial economy. The financial economy [financial asset’s prices like the S&P 500] should reflect the state of the physical economy. To be more specific, financial markets are forward looking and therefore are supposed to reflect the consensus of what the condition of the physical economy will be in the future given today’s known physical economic variables/indicators. There is still supposed to be that linear/fundamental relationship between the state of the physical economy, on a forward-looking basis, and the current financial economy. That link from the physical economy to the financial economy can dislocate and during bubbles this dislocation grows very large – to the point where the financial economy is moving on a small number of economic variables, ignoring the majority, and sometimes even moving not based on the physical economy at all. At this point, in my opinion, the only thing that can burst the bubble is a large physical economic shock that forces the financial economy to move out of the non-fundamental world it is living in and brings it back to reality. On this note, we know that Covid-19 provided the physical economic shock. However, was there a financial economic leading indicator which could have tipped us off before the sharp sell-off in the traditional asset classes?

Dry Bulk Market Overview

The shipping industry is an extremely important cog within the commodity market’s supply and demand chain. This industry enables supply centers to get their product to demand centers. Shipping is separated into wet and dry bulk. The following overview uses 2017 industry figures.

The three largest bulk shipping commodities are iron ore (29%), grains (10%) and coal (23%).There are about 11,000 vessels in the world’s dry bulk fleet and each dry bulk carrier has a useful life of about 25 years. China dominates the dry bulk trade accounting for about 40% of major dry bulk goods and greater than 70% of iron ore trade. Japan and South Korea account for more than 25% of global coal imports. India has been experiencing increasing demand [four-fold] over the past decade and Europe’s demand has remained relatively stable. From 2000 to 2017, dry bulk trade has had a CAGR of 4.6%. Brazil and Australia are the two main iron ore exporters – combined they account for about 82% of global iron ore exports. The most important shipping route is from Brazil to China as it takes almost 3 times as long to get there versus the Australia to China route. China accounts for about 75% of iron ore imports, 20% of coal imports and is the world’s largest importer of soybeans. On the industry infrastructure supply side, China also accounts for about 40% of the global shipbuilding market. Clearly, China is the most important cog in what is the industry that allows commodity markets to function effectively.

Baltic Exchange Dry Index

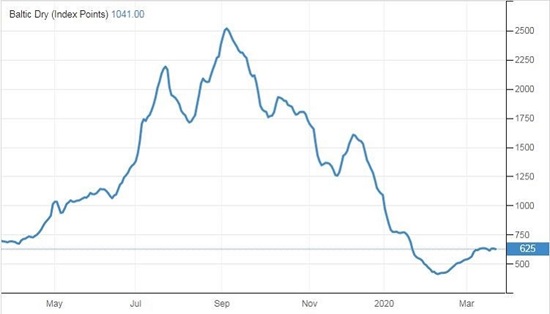

The Baltic Dry Index (BDI) is a shipping index which measures changes in the cost of transporting various raw materials across more than 20 routes for each of the BDI component vessels. The BDI is calculated daily and provided by the Baltic Exchange reflecting average spot prices for dry bulks shipped globally. The BDI reached an all-time high of 11,793 in in May 2008 and an all-time low of 290 in February 2016.

According to capital.com, the recent BDI high of around 2510 in September 2019 was due to ‘front-running’ the upcoming tariffs in the US-China trade war. The BDI started dropping afterwards and from November onwards, the BDI news was all down to China and Covid-19. China’s first reported case of Covid-19 was around mid-November. The spread of Covid-19 was exponential and lead to a sharp economic slowdown. Given China’s importance within the shipping industry, the Chinese economic impact was seen through the BDI. The new year brought a significant drop in the index with early February seeing the low of around 410. There was around an 80% drop from the September 2019 to February 2020.

Baltic Exchange Dry Index 1-year Chart

Source: https://tradingeconomics.com/commodity/baltic

The broad-based sell-off in equity markets didn’t start until the end of February, which is about half a month after the BDI’s 80% drop. This meant that there was a significant drop over a 3-month period in the BDI which followed another 2-week lag before the broad-based equities sell-off occurred. The reason for the isolation of the extreme drop is due to China’s major presence within the dry bulk market and the isolation of Covid-19 in China and neighboring countries. While Covid-19 primarily stayed within China, the other asset classes and markets essentially disregarded it. For those paying attention, due to the BDI drop, you could see the physical economic impact (as shown by the Dry Bulk Index) that Covid-19 had on the financial economy. It was not until Covid-19 started spreading across countries and continents did the other asset classes/financial economies start dropping as the economic impact Covid-19 brought was the same that the shipping industry felt when Covid-19 was just impacting China. One could infer that China is the benchmark country to see how long it takes Covid-19 cases to start decreasing and economic activity to start picking up again to get an idea of how long other countries will be feeling the significant economic impact of the pandemic.

I have been asked why traditional asset classes, including commodities, have been moving together. There have been a few studies into this increased correlation since the GFC but, from a high-level, I hypothesize that due to the artificial bubbles that were created, there was a severe dislocation between the physical economy and the financial economy. The traditional market drivers didn’t move the markets anymore, an example being company earnings in the equity markets; it didn’t really matter what company earnings were. With each financial economy’s idiosyncratic drivers becoming less and less important, there was an increased weighting of the macro drivers; these macro drivers have an effect on most markets. Essentially, beta [macro/market risks] engulfed alpha [micro/idiosyncratic risks] within each traditional asset class which led to an increased correlation of the traditional asset classes due to the overlap of macroeconomic risks associated with each market. Covid-19 brought to light the fundamental overlapping macroeconomic relationships of the traditional asset classes and gave us a look at the power of globalization which can be seen through the speed of the pandemic across the globe.

**********

Karl Rogers is Founder of ACE Capital Investments

Investment programs involve substantial risk, including the complete loss of principal, and no assurance can be given that the Fund’s investment objectives will be achieved. Past returns are no guarantee of future results.

None of the contents should be considered as advice or a recommendation to investors or potential investors in relation to holding, purchasing or selling securities or other financial products or instruments and does not take into account your particular investment objectives, financial situation or needs. Before acting on any information you should consider the appropriateness of the information having regard to these matters, any relevant offer document and in particular, you should seek independent financial and legal advice. Statements of opinion and recommendation will be introduced as such and generally reflect to judgement or opinion of Karl Rogers. These opinions may change at any time without written notice and ACE Capital Investments assumes no responsibility to send updates regarding any changes.

This document may not be reproduced in whole or in part, and may not be delivered to any person without the prior written consent of the author.

Any references to product(s) offered by ACE Capital Investments is not an offer to sell, or a solicitation of an offer to buy, a partnership interest in any fund described herein. No such offer or solicitation will be made prior to the delivery of the applicable offering memorandum and other materials relating to the matters mentioned herein. No representation or warranty is made by any fund or any other person (including any of its agents or other representatives) as to the accuracy or completeness of the information contained herein. Only those particular representations and warranties which may be made in definitive agreements relating to the funds, when, as and if executed, and subject to such limitations and restrictions as may be specified in such definitive agreements, shall have any legal effect.

The information contained herein was taken from financial sources that were deemed to be reliable and accurate at the time of publication. Changes in the market may cause this information to become out-dated or obsolete.

Neither Karl Rogers or ACE Capital Investments are affiliated with, or endorse, sponsor, or recommend any product or service advertised herein, unless otherwise noted.

***

The views expressed in this article are those of the author and do not necessarily reflect the views of AlphaWeek or its publisher, The Sortino Group

© The Sortino Group Ltd

All Rights Reserved. No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or scanning or otherwise, except under the terms of the Copyright, Designs and Patents Act 1988 or under the terms of a licence issued by the Copyright Licensing Agency or other Reprographic Rights Organisation, without the written permission of the publisher. For more information about reprints from AlphaWeek, click here.